Demand for physician services is rising on multiple fronts. Visits per provider are at decade highs, primary care searches are reversing course, and remote monitoring has moved into mainstream practice. The next 18 months will be defined by which practices translate this demand into capacity without burning out their teams.

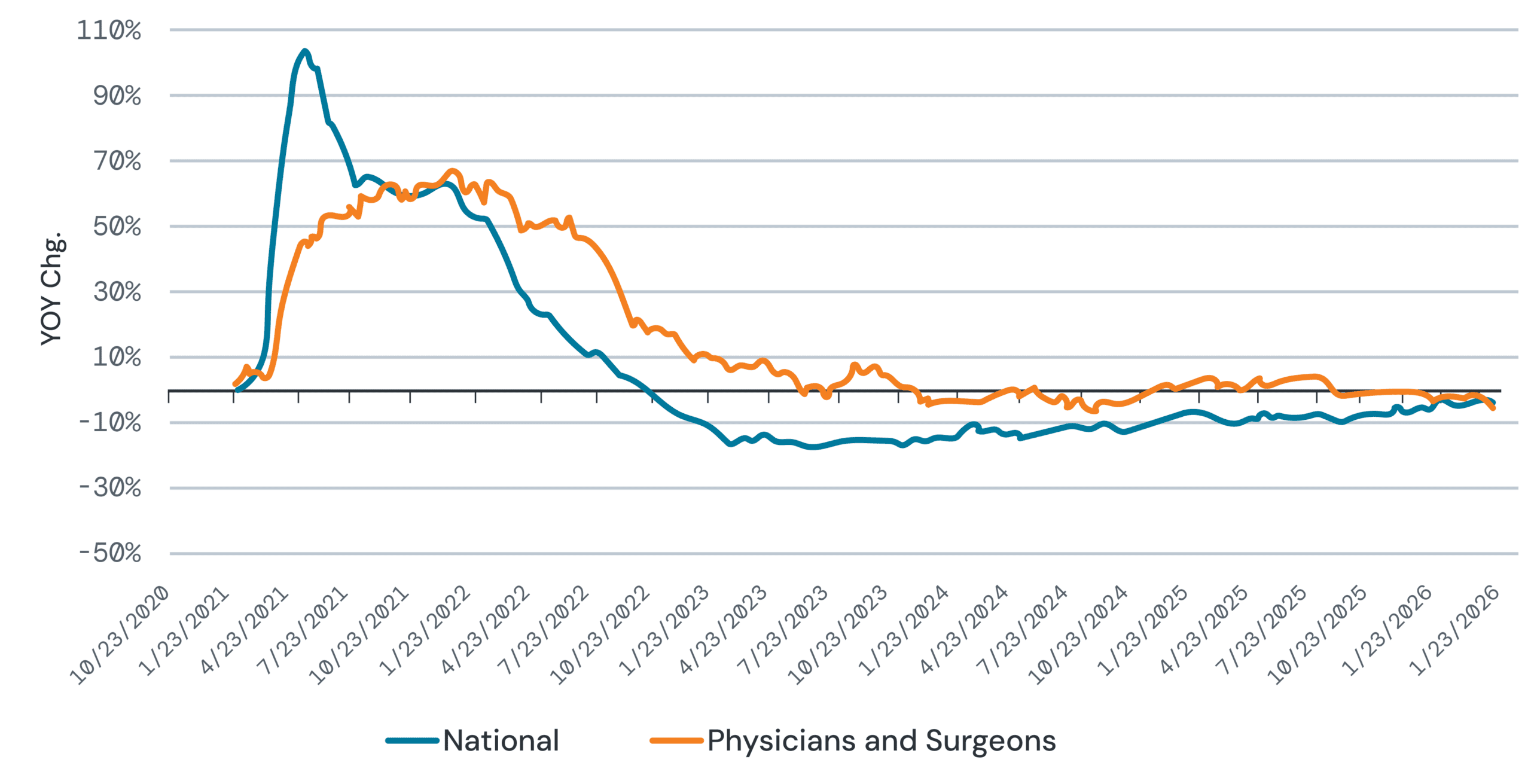

1. Physician Job Postings Have Flatlined—And That’s Not a Bad Thing.

The post-pandemic hiring frenzy is a distant memory. Job postings for physicians and surgeons have tracked near the zero line for over two years. We now see physician-specific and national trends have a slight negative year-over-year readings, which means the hiring frenzy of 2021 and 2022 has fully recalibrated.

Indeed.com Job Postings for Physicians and Surgeons

Source: Indeed.com

Key takeaway: A flat hiring market is good news for practice owners. Even though recruiting timelines are quite predictable, bidding wars are over, and you can focus on finding the right fit rather than racing to fill seats. This stability will enable you to be more selective and invest in onboarding and culture.

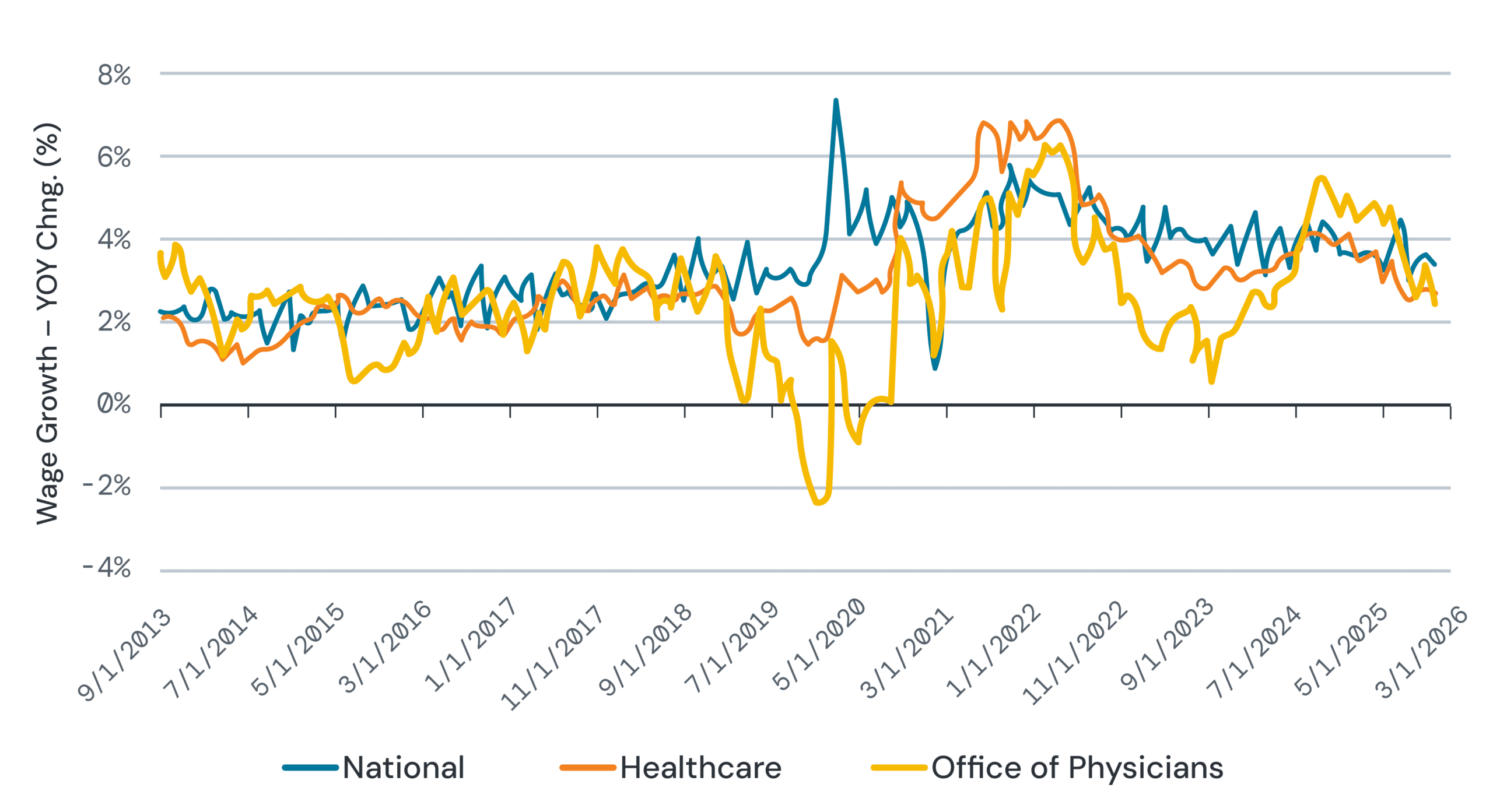

2. Wage Growth Is Converging, but Physicians’ Offices Still Run Hot.

After a few turbulent years, wage growth across the national economy, specifically in the healthcare and physicians’ offices is now converging in the 3–5% range. The wild divergences of 2020–2022, when physician office wages swung from -3% to over 5% within months, have given way to more predictable increases. That said, physician office wages remain slightly more volatile and tend to run at the high end of the range, reflecting ongoing competition for clinical talent.

Wage Growth

Source: Bloomberg Finance, L.P.

Key takeaway: The 3–5% annual payroll budget becomes the new normal, but don’t try to win the talent war on salary alone. The smartest practices are competing on total compensation, such as flexible scheduling, CME support, mentorship programs, and a culture that keeps people from looking elsewhere.

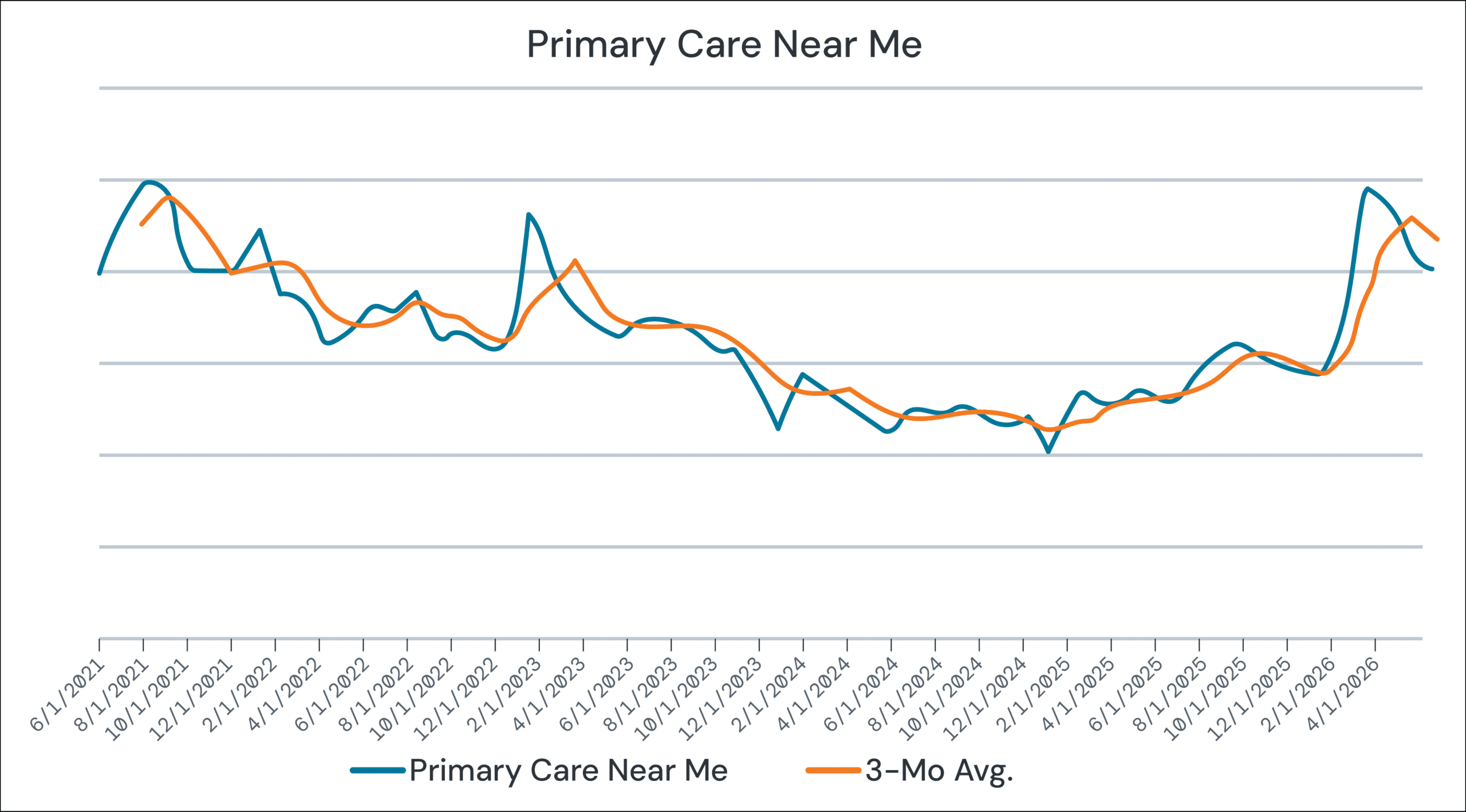

3. Patients Are Searching for Primary Care Again.

After a multi-year decline from the 2021 peak, Google searches for “primary care near me” are bouncing back. The 3-month average has climbed sharply since late 2025, and recent readings are approaching levels not seen since early 2022. This is a meaningful reversal of the downtrend that dominated 2023 and 2024, when patients had simply stopped shopping for new providers online.

Google Trends: “Primary Care Near Me”

Source: Google Trends

Key takeaway: Patients are actively looking for providers again. This is your opportunity to make sure your practice shows up when they search. Review your online presence, Google Business Profile, website, and patient reviews, and make it easy for new patients to book. The practices that invested in digital visibility during the quiet period are now reaping the benefits.

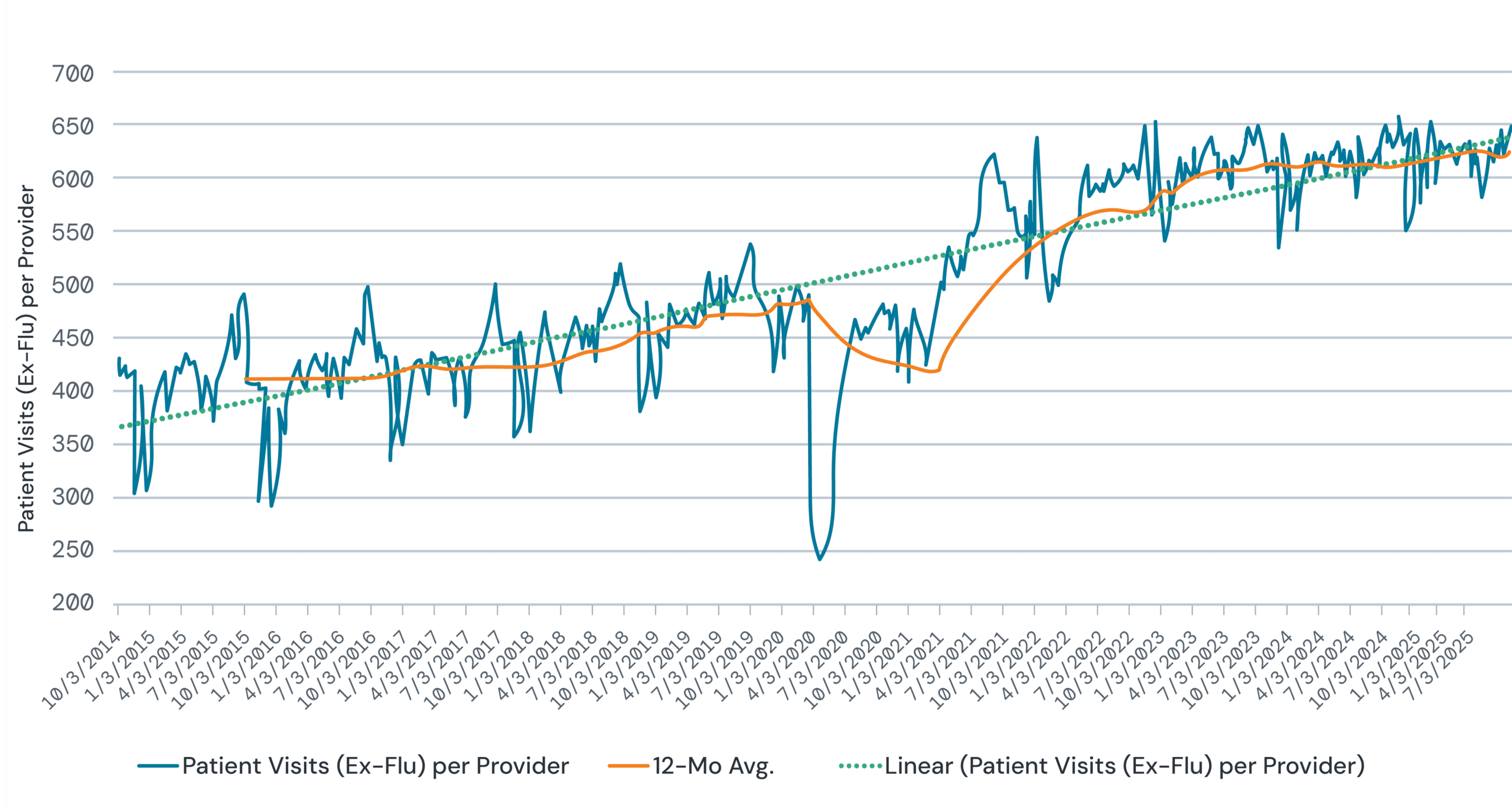

4. Patient Visits Continue to Climb.

Patient visits per provider (excluding flu) continue a decade-long upward march. The 12-month moving average is now firmly around 600 visits per provider, up from roughly 400 in 2014. Even after the dramatic COVID dip in 2020, the recovery was swift, and the trend has only accelerated. The linear trendline shows no sign of slowing down, and the demand for in-person care is as strong as it’s ever been.

Patient Visits

Source: Centers for Disease Control and Prevention

Key takeaway: The patients are consistently showing up, and in growing numbers. This is a great time to invest in operational efficiency, including scheduling systems, support-staff ratios, and mid-level providers to help manage the workload. Strong demand is a gift, but only if your operations can keep pace without burning out your team.

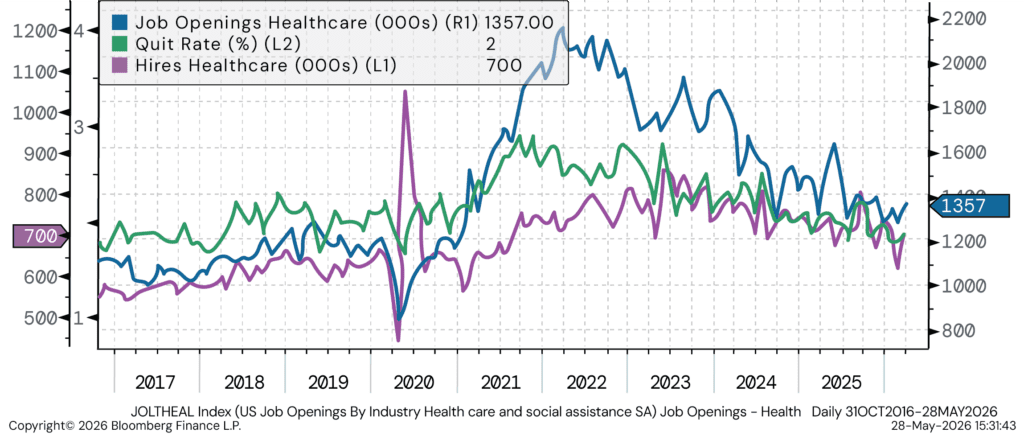

5. Healthcare Job Openings Are Climbing Again, While Quit Rates Stay Low.

The healthcare jobs picture has an interesting wrinkle heading into mid-2026. Job openings have ticked back up to around 1.36 million, rising modestly from their post-2022 lows. At the same time, quit rates remain near historically low levels at roughly 2%, and hires have stabilized around 700,000. In plain English: more positions are available, but workers are staying put, and employers are filling roles at a steady clip.

Source: Bloomberg Finance, L.P.

Key takeaway: Low quit rates are a strong signal that retention efforts are working, so keep doing what you’re doing. But with openings ticking higher, the competition for new hires hasn’t disappeared. It is recommended to maintain your recruitment pipeline, and remember that the best defense against turnover is a workplace people don’t want to leave: career paths, mentorship, and a culture of respect.

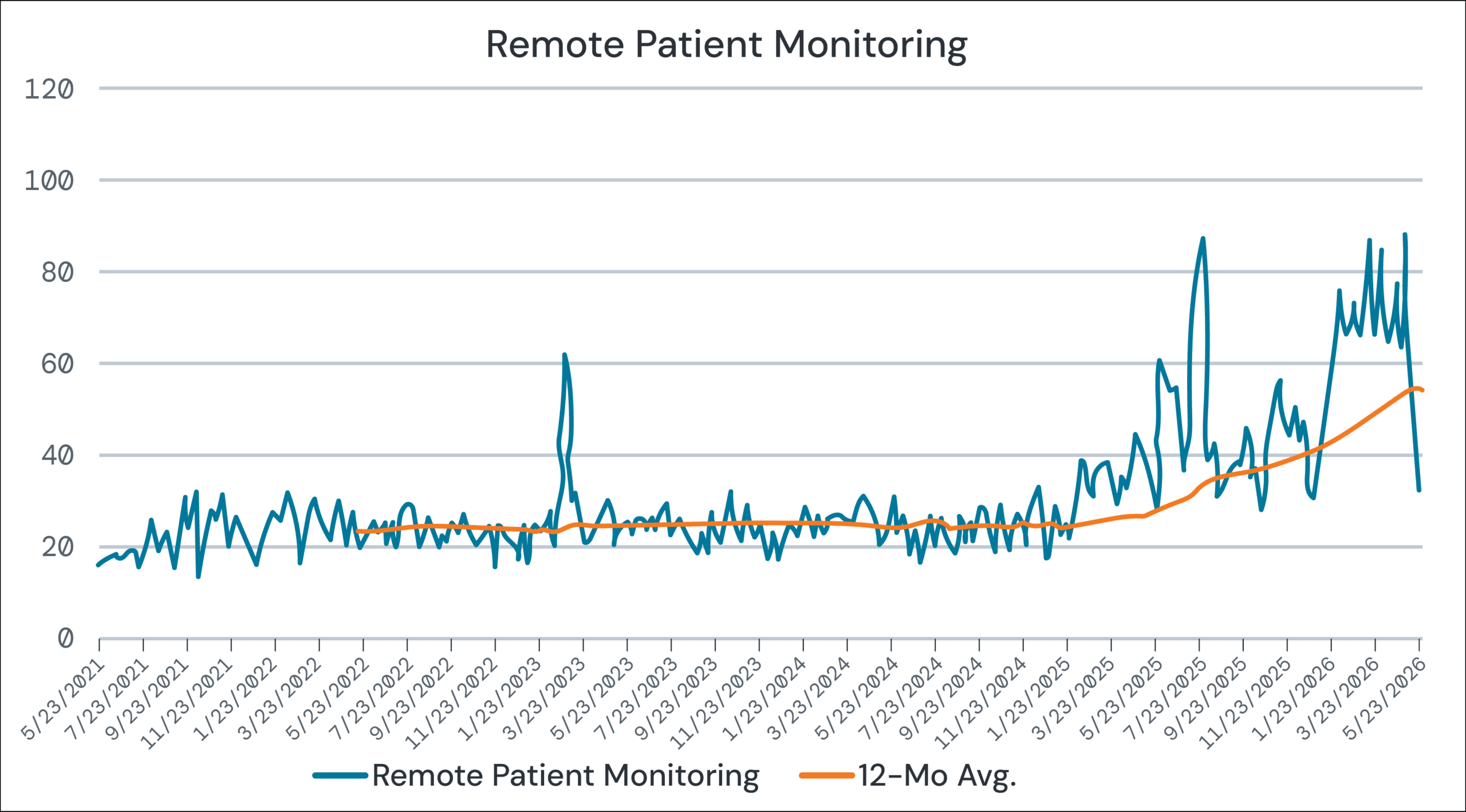

6. Remote Patient Monitoring Has Gone from Trend to Tidal Wave.

This is the chart that should get your attention. Google Search interest in “remote patient monitoring” was essentially flat from 2021 through mid-2025, hovering around 20–25 on the index. We see an increase in interest in “remote patient monitoring” in late 2025, and recent weekly readings have spiked to 80, 90, and even 100—levels never before seen. The 12-month average has nearly tripled, rising from 25 to around 60. This isn’t a blip; it is a structural shift in how providers, patients, and the industry think about care delivery.

Source: Google Trends

Key takeaway: Remote monitoring is no longer an experiment; it’s becoming the standard of care for chronic condition management. If your practice hasn’t evaluated RPM platforms yet, you’re falling behind. The upside is real: better patient outcomes, new billable services (think chronic care management and remote physiologic monitoring codes), and a competitive edge in attracting patients who expect modern, tech-enabled care. Start with one chronic condition, such as hypertension or diabetes, and build from there.

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the publication date and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Certain investor qualifications may apply. Definitions for Qualified Purchaser, Qualified Client and Accredited Investor can be found from multiple sources online or in the SEC’s glossary found here https://www.sec.gov/education/glossary/jargon-z#Q