U.S. manufacturing has been in expansion territory for five consecutive months, signaling that this recovery might have staying power. But this growth is being fueled by productivity not hiring. Output is increasing even as headcount declines, input costs remain elevated across the board, and skilled factory workers continue to command premium wages. Manufacturers who invested early in automation, employee retention, and cost discipline are widening their lead. The big question for the remainder of 2026 is whether companies can maintain pricing power and workforce strategies strong enough to protect margins as demand picks up.

1. Expansion Mode is Back in Manufacturing and Productivity is Doing the Work

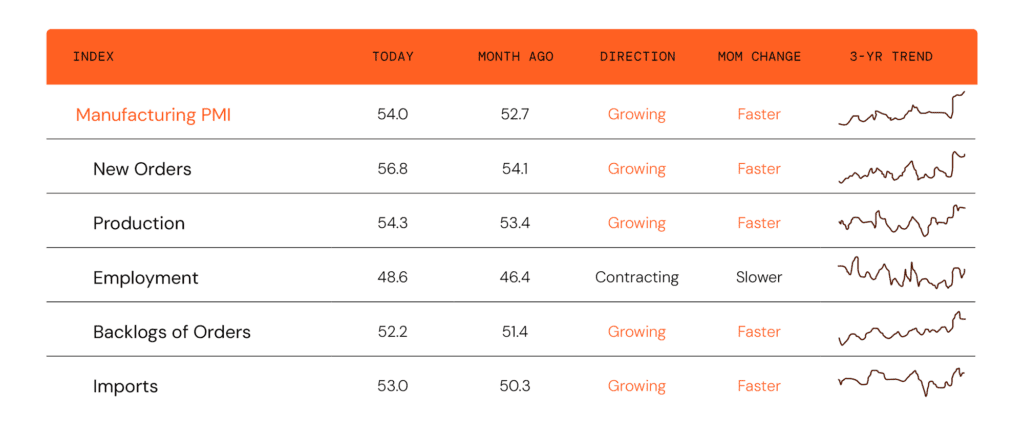

ISM Snapshot

Source: Institute of Supply Management (ISM)

The headline Manufacturing PMI rose to 54.0, marking the fifth consecutive month of expansion and its strongest reading since early 2023. New Orders accelerated to 56.8, Production held steady at 54.3, and both Backlogs (52.2) and Imports (53.0) remained in growth territory. Overall, factory activity is building, orders are filling, and manufacturers are bringing in materials to keep up with demand.

The one notable weak spot is Employment, which came in at 48.6. While still in contraction, it continues to improve and demonstrates how factories are increasing output even as headcount declines.

What this means for you: This is the kind of expansion manufacturers have been waiting for. Output is climbing while headcount shrinks, highlighting that this cycle is powered by productivity and automation rather than labor growth. Manufacturers who invested in technology, efficiency, and lean operations over the past two years are beginning to see those decisions pay off now. This type of recovery rewards efficiency and widens the gap between disciplined operators and everyone else each quarter. The key takeaway: the cost of waiting grows with every month you don’t. So, keep investing in automation and process improvement to stay competitive as the cycle gains momentum.

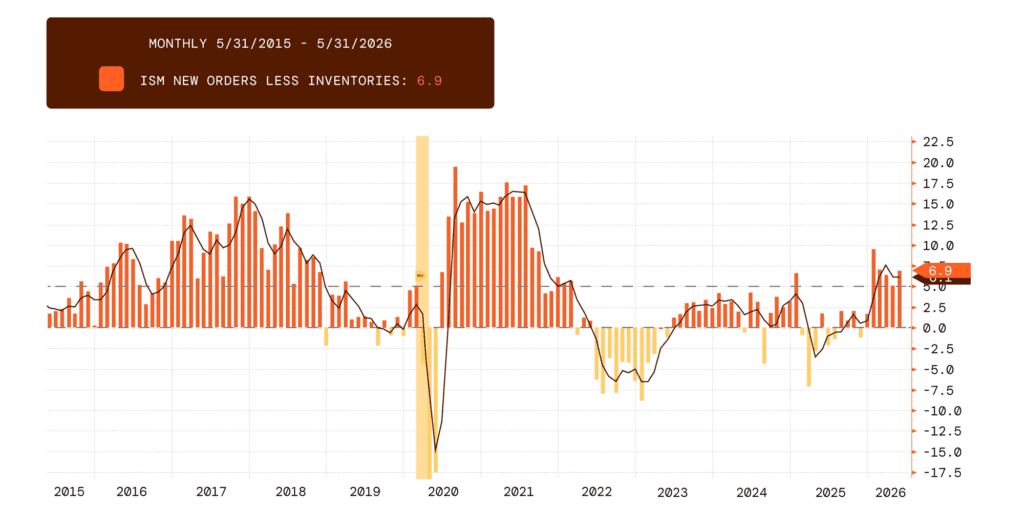

2. New Orders are Outpacing Inventories — a Strong Demand Signal

Source: Bloomberg Finance, LP

The ISM New Orders less Inventories reading climbed to +6.9, extending a run of several positive readings after spending most of 2024 and 2025 near zero or in negative territory. Historically, sustained strength in this measure has been one of the most reliable leading indicators of broader manufacturing expansion.

What this means for you: This is one of the most important charts we watch, and right now it’s telling a clear story: demand is starting to outpace supply. Inventories that were built up cautiously over the past year are now being worked down, while new orders continue to pull ahead. The wait-and-see approach has run its course. Now is the time to review production capacity, pressure-test supplier lead times, and identify the SKUs most at risk if demand keeps accelerating. For high-demand product lines, selective restocking makes sense. The window to prepare for a sustained upturn is open now.

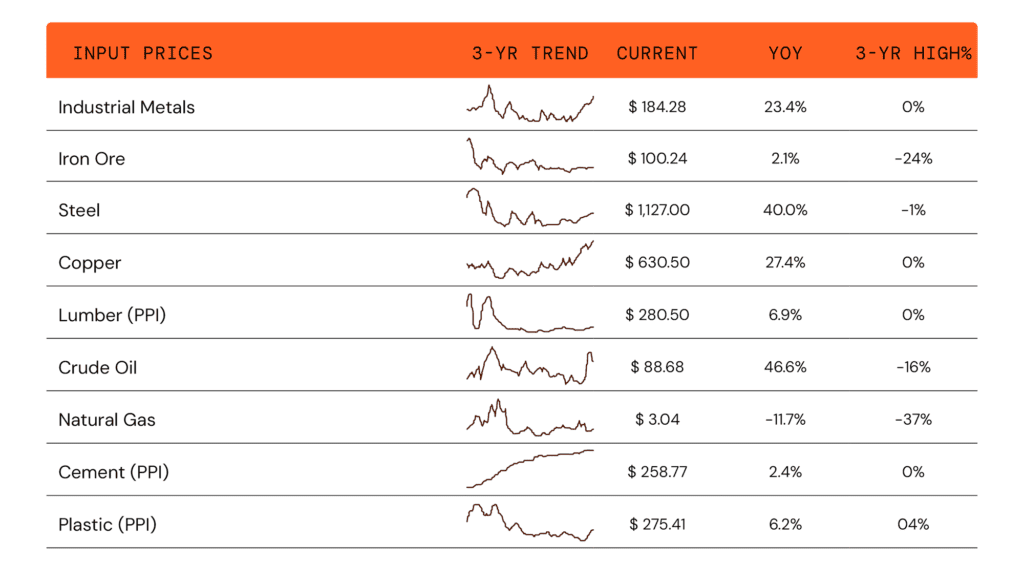

3. Input Costs are Surging, and the Pressure is Broad-Based

Source: Bloomberg Finance, LP

Input costs are rising sharply across nearly every major category. Steel prices are up 40% year-over-year and now sits near a three-year high. Copper has climbed 27%, driven by demand from electrification and AI infrastructure buildouts, while industrial metals overall are up 23%. Crude oil has surged 47%, though it remains 16% below its three-year peak. Lumber (+7%), cement (+2%), and plastics (+6%) have also moved higher. But the lone outlier is natural gas, which is down 12% year-over-year and remains 37% below its three-year high, offering some much-needed relief for energy intensive operations.

What this means for you: This is one of the biggest challenges manufacturers are facing right now. Almost every major input category is up, and several are at or near multi-year highs. More importantly, the pressure appears to be structural, driven by long-term forces such as electrification, infrastructure, and capacity buildouts, areas that will likely not unwind quickly. In this type of environment, margin discipline will be critical in 2026. Review which cost increases have been passed through to customers and which are still being absorbed internally. If your operations depend heavily on steel and copper, now is the time to evaluate forward contracts or strategic pre-buys at current levels. For energy-intensive operations, locking in natural gas rates while prices remain favorable could provide a meaningful advantage. When building 2026 budgets, use current input prices as your baseline, not last year’s.

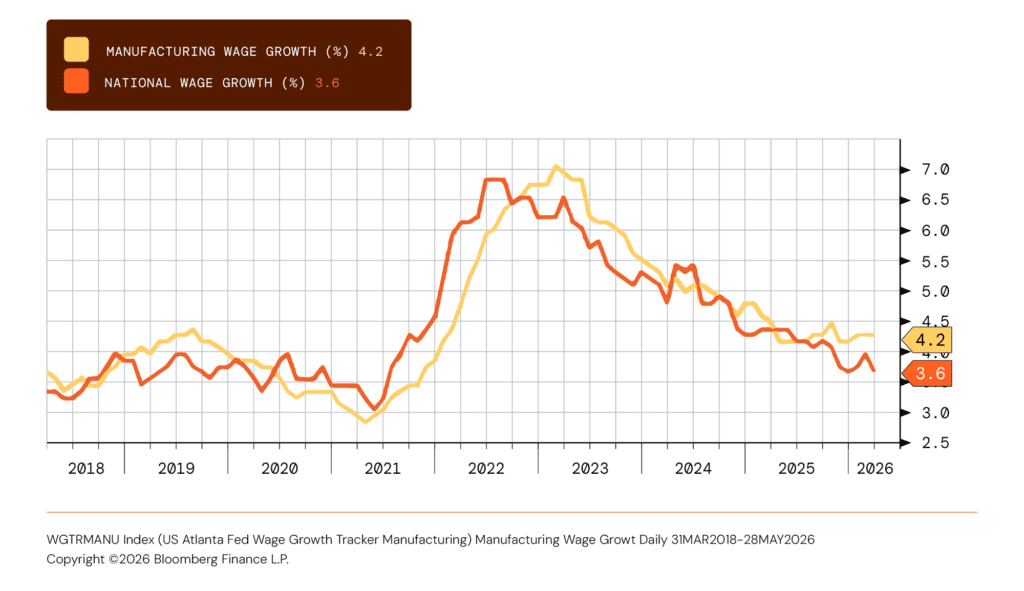

4. Manufacturing Wages are Outpacing the National Average

Source: Bloomberg Finance, LP

Manufacturing wage growth has climbed to 4.2% year-over-year, placing it above the national average. This gap has widened steadily since mid-2024, reversing the pattern seen in 2022 and 2023 when wage growth was led by services and hospitality. Even as overall manufacturing employment continues to contract, demand for skilled factor floor labor remains in high demand.

What this means for you: This is the labor squeeze many manufacturers are feeling in real time: you need fewer workers overall, but the talent you do need is becoming more expensive. The wage premium is concentrated in the skilled roles that modern manufacturing industry increasingly depends on — maintenance technicians, controls specialists, and highly trained production talent. In this market, retention is often far less costly than replacement. Focus compensation, training, and career path investment toward your highest-value technicians and operators. At the same time, use automation where it makes sense to reduce wage pressure in lower-skill, repetitive roles.

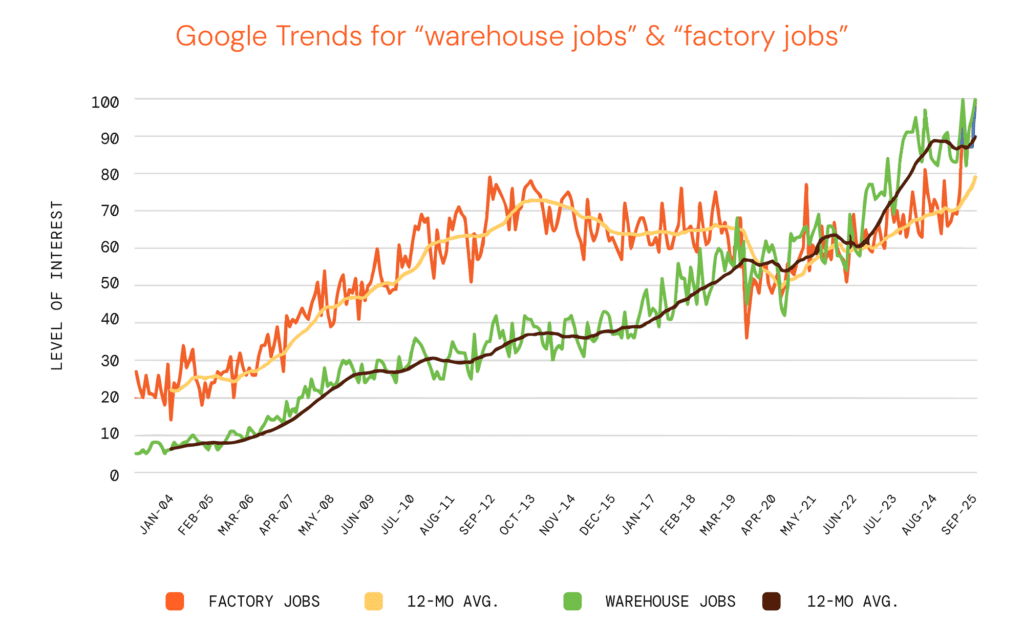

5. Workers are Searching for Factory and Warehouse Jobs at Record Levels

Source: Google Trends

Google search interest for “warehouse jobs” and “factory jobs” has reached its highest level since tracking began in 2004. The 12-month moving averages for both terms has climbed sharply since late 2024, pointing to a growing pool of workers actively seeking employment opportunities in manufacturing and distribution.

What this means for you: There’s a silver lining in the wage pressure story: labor supply is beginning to respond. Increased attention on reshoring, the rising visibility of the manufacturing industry’s recovery, and frustration with pay in gig and service-sector roles are all drawing more workers toward industrial roles. Now is the time to strengthen your employer brand. Step up recruiting efforts, build partnerships with local trade schools and community colleges, and clearly communicate career pathways for new hires. Manufacturers that move quickly will be in the best position to build their skilled bench before competitors do.

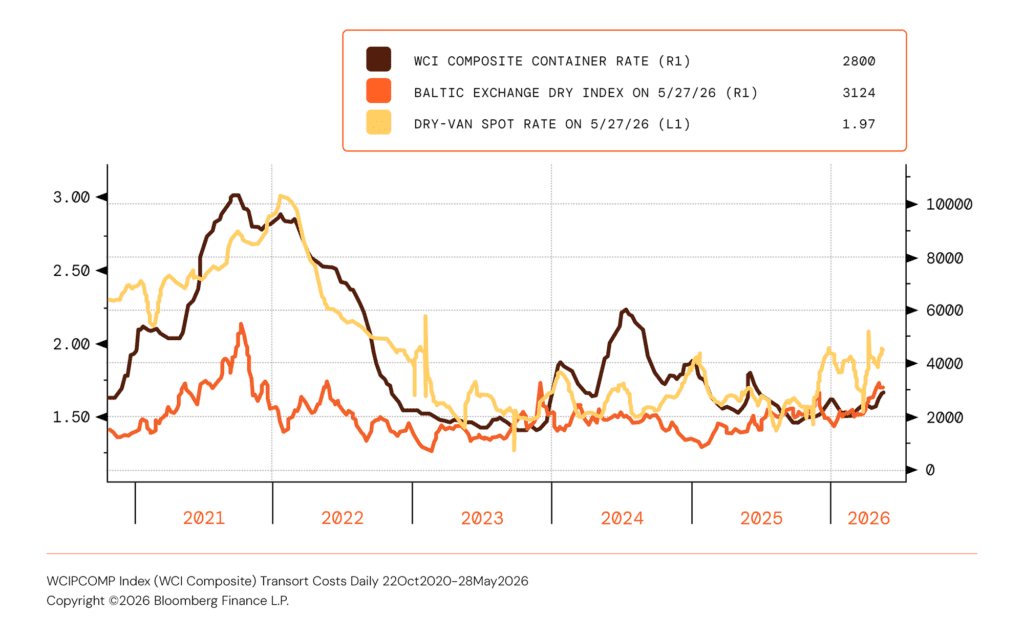

6. Freight Markets are Sending Mixed Signals

Container and Truck Rates

Source: Bloomberg Finance, LP

Freight markets continue to send mixed signals. The WCI Composite Container Rate is holding at $2,800, relatively stable and well below the 2021 and 2022 crisis highs, but still above pre-pandemic norms. Meanwhile, the Baltic Exchange Dry Index has climbed to 3,124, reflecting strong global demand for iron ore, coal, and grain. By contrast, the Dry Van Spot Rate has dropped to $1.97 per mile and remains near multi-year lows, suggesting domestic trucking capacity is ample while freight demand is soft relative to available trucks.

What this means for you: The broader signal is encouraging as global industrial demand remains healthy, supported by AI infrastructure buildouts and supply chain shifts. That is a positive backdrop for manufacturers with international exposure. However, domestic logistics may offer the clearest opportunity. Low Dry Van Spot Rates are giving shippers more negotiating leverage, making this a favorable window to secure competitive transportation rates for domestic distribution. Maintain flexibility across the ocean, rail, and truck routes so you can adjust quickly as these markets continue to move in different directions.

This commentary is brought to you by Aprio advisors. If you have any questions, connect with our team today.

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the publication date and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Certain investor qualifications may apply. Definitions for Qualified Purchaser, Qualified Client and Accredited Investor can be found from multiple sources online or in the SEC’s glossary found here https://www.sec.gov/education/glossary/jargon-z#Q