Executive Summary

- Inflation, inflation, inflation: That is what has been on the market’s mind over the past week, as economic data signaled that inflation is coming in faster than expected, while growth stocks sold off on the news.

- Expect the unexpected: Dollar stores may be the unlikely beneficiary of consumers’ frayed nerves; meanwhile, employers are asking: “Does anyone want a job?”

To discuss your current investment strategy, schedule a consultation with an Aprio advisor.

In the Markets

Like “Bennifer,” stone-washed jeans and DIY projects, things go in and out of style.

Stock markets are no different.

What’s out? Growth stocks with expectations of huge future cash flows, where there’s little today.

Expectations of cash flow growth rates determine how stock prices fluctuate. When investors believe cash flows will come in above expectations, prices increase … and vice versa. Recent announcements from fast-growing companies have been disappointing in this area.

A leading index of SaaS/cloud companies[1] has declined ~25% since its February peak and nearly 15% in the last month. Concerns about growth and higher interest rates have hit prices.

Meanwhile, the special-purpose acquisition company (SPAC) craze is going out of style for investors — at least when it comes to their IPOs and stock prices. The IPOX SPAC Index is off 24% since its February peak for similar reasons. There were 300 SPAC mergers in the first quarter of 2021, yet just 10 deals were announced in April (as of this article’s writing). Bloomberg notes that electric vehicle SPACs have lost $40 billion of their $60 billion valuations (link).

In a week of red, the growthier Nasdaq and Russell 2000 indices underperformed and are down for May.

What’s working? The strongest performers last week were the steady-eddy revenue industries, such as utilities, consumer staples and real estate — they were more predictable with lower expectations.

In the Economy

It’s getting hot in herrrre…

It was a big, big week for economic data — especially around inflation, which is the topic du jour.

For several months, we’ve noted how inflation has been popping up in the headlines and data; and last week, it was in the macro economic data and increasing faster than most anticipated.

The Consumer Price Index (core, excluding food and energy) increased 0.9% from March, three times as fast as analysts were expecting and compared to the prior month. April’s results annualize to an 11% growth rate; compared to April 2020, prices are up 4.2%.

The Producer Price Index — which looks at costs between businesses — increased at two times the rate of expectations and at nearly a 9% annual rate.

A significant reason for the higher prices is shipping costs: container prices have doubled from pre-COVID levels and spiked again this quarter.

Shanghai to Los Angeles Container Shipping Rates

Jun. 2016 – May 2021

Part of the challenge is that employers can’t fill job openings. We heard it in comments from companies in prior weeks and we saw it in the data again last week.

The JOLTS Job Openings Survey reported 8.1 million openings last week, about 8% higher than expected and nearly 800,000 more than in March. For small businesses, job openings have been hard to fill, at record levels going back to the early 1970s.

Small Business Job Openings

Dec. 31, 1973 – Apr. 30, 2021

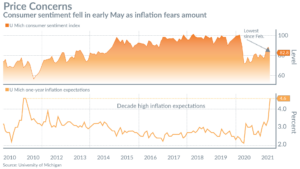

The jump in inflation may be hitting consumers’ hearts and minds already.

There’s something about Friday

For the second consecutive Friday, we had an economic shock. Two weeks ago, it involved employment; last week, it involved retail sales.

Retail sales in April missed estimates by a country mile. Excluding auto and gas, they declined 0.8%, when economists expected growth of 0.3%, and were down from March’s 8.9% (thank you, stimulus checks).

Meanwhile, concerns about inflation are top of mind for consumers.

The University of Michigan’s Consumer Sentiment Survey was nearly 10% below estimates, lower than the most pessimistic of economists’ expectations in a Bloomberg survey. A big reason for this drop is … you guessed it, spiking concerns about inflation.

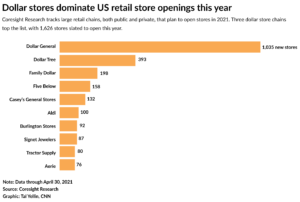

What might be a beneficiary of inflation? Dollar stores

If more customers feel a pinch in their wallets, purchasing smaller-sized, lower-price-point items could accelerate that.

According to a CNN Business article[1] citing Coresight Research, nearly one in three new store openings in the United States is a Dollar General:

The growth of dollar store openings would reflect a “K”-shaped economic rebound and the slow jobs recovery.

A Few Stories That Caught My Eye

- Is the super-controversial, Twitter-loving SPAC King getting his comeuppance? (link)

- Daily Double: We’re looking at Elon Musk’s impact on Dogecoin (link) and Bitcoin (link) this week.

- The group that hacked the Colonial Pipeline and forced its shutdown has shut down itself. (link)

[1] Nathaniel Meyersohn, “Nearly 1 in 3 new stores opening in the US is a Dollar General,” CNN Business, May 6, 2021, accessed May 2021.

[1] Bessemer Venture Partners Nasdaq Emerging Cloud Index

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the current date (May 17, 2021) and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Securities offered through Purshe Kaplan Sterling Investments. Member FINRA/SIPC. Investment Advisory Services offered through Aprio Wealth Management, LLC, a registered investment advisor. Aprio Wealth Management, LLC and the Aprio Group of Companies are not affiliated with Purshe Kaplan Sterling Investments.