Real estate investors are navigating a shifting landscape as tight cap rate spreads, with rising borrowing costs and maturing debt complicating investment strategies. Liquidity is improving in select asset classes, but price discovery remains a challenge. Multifamily and industrial show resilience, despite rising concessions and moderating rent growth. Leading indicators of future supply point to easing future pressures, creating opportunities for well-positioned assets and those with a long-term outlook.

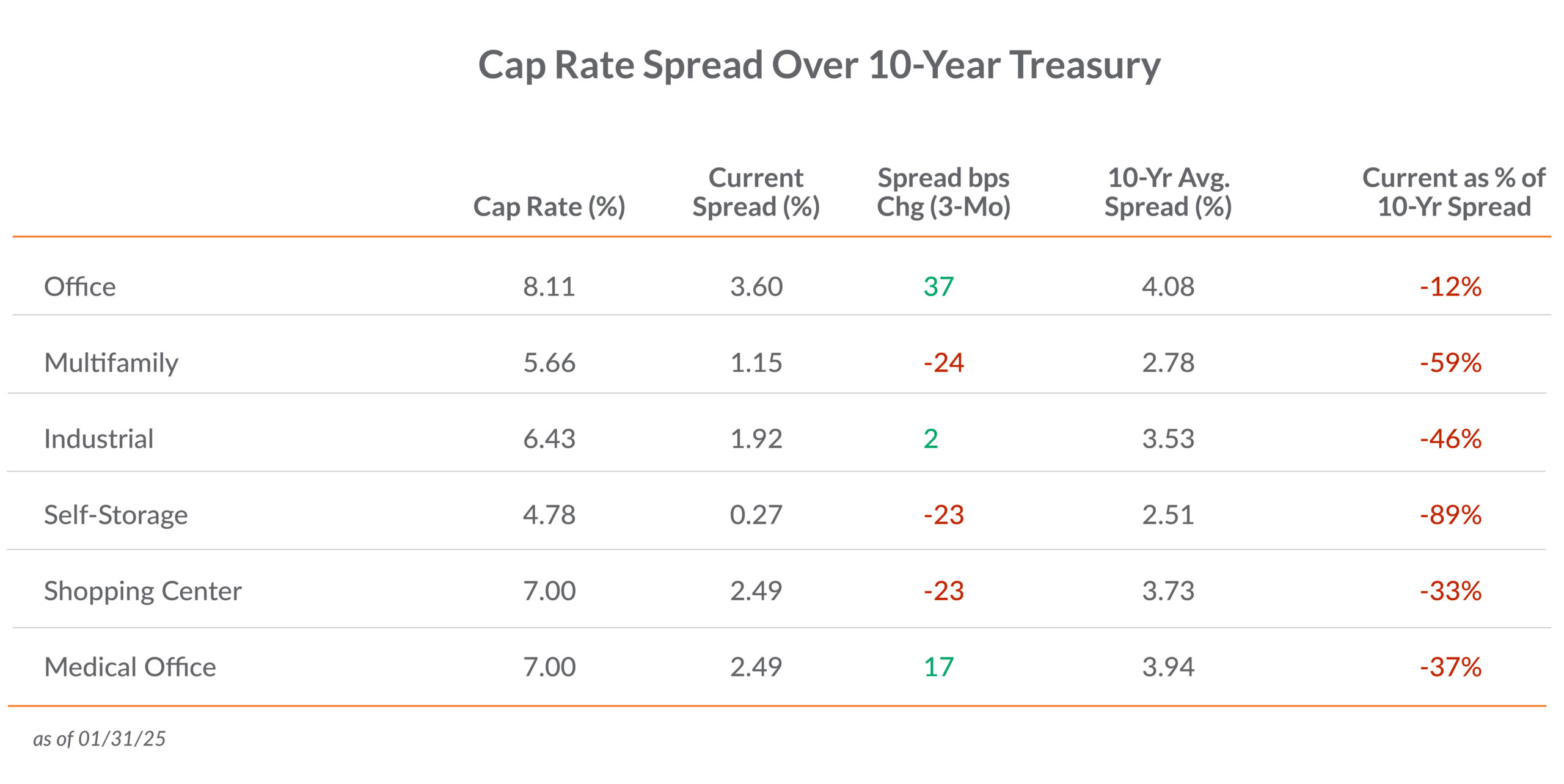

1. Cap Rate Spreads Remain Tight Across Most Sectors

Source: RCA, NAREIT, & ICA Data Indices, LLC

The spread between cap rates and the 10-Year Treasury yield remains below historical averages, reducing real estate’s appeal relative to bonds and other assets. While office cap rates have slightly expanded, multifamily, self-storage, and shopping centers face tighter spreads, heightening competition for capital as fixed income offers more competitive risk-adjusted returns.

What this means for you:

Investors need to be highly selective in their real estate allocations, prioritizing properties with strong cash flows and value-add potential. While offices and shopping centers provide higher cap rates, they also carry operational risks such as fluctuating tenant demand and leasing challenges. Multifamily remains attractive but it requires a focus on markets with sustainable rent growth. While industrial properties offer stability, they may see rent growth moderation as supply expands.

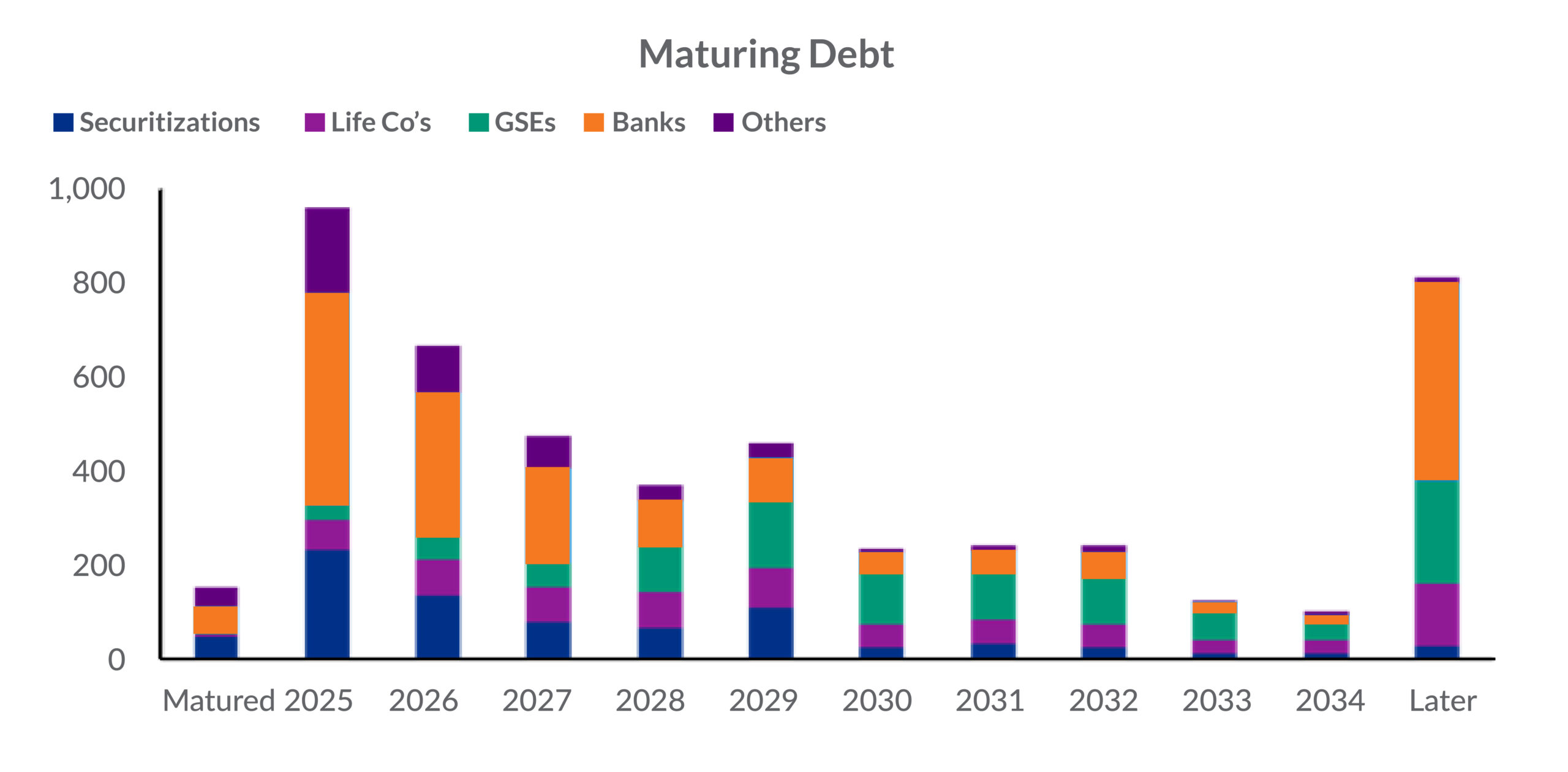

2. Maturing CRE Loans Present Financing Challenges

Source: Cohen & Steers

A wave of commercial real estate debt maturities is approaching, with 2025 presenting a significant refinancing challenge. Rising interest rates and shifting bank regulations are straining liquidity. Banks, life insurance companies, and securitized lenders are facing balance sheet constraints, potentially resulting in higher costs for borrowers. Distressed sales and loan modifications may increase, particularly in struggling asset classes.

What this means for you:

Real estate asset owners with near-term maturities should explore refinancing options, including with alternative financing sources, such as private credit and joint ventures. The lending environment is dramatically different from when many loans were previously originated, so expect more adverse terms. Those looking for distressed opportunities should focus on good properties with over-leveraged balance sheets, thus sellers may be forced to accept discounts.

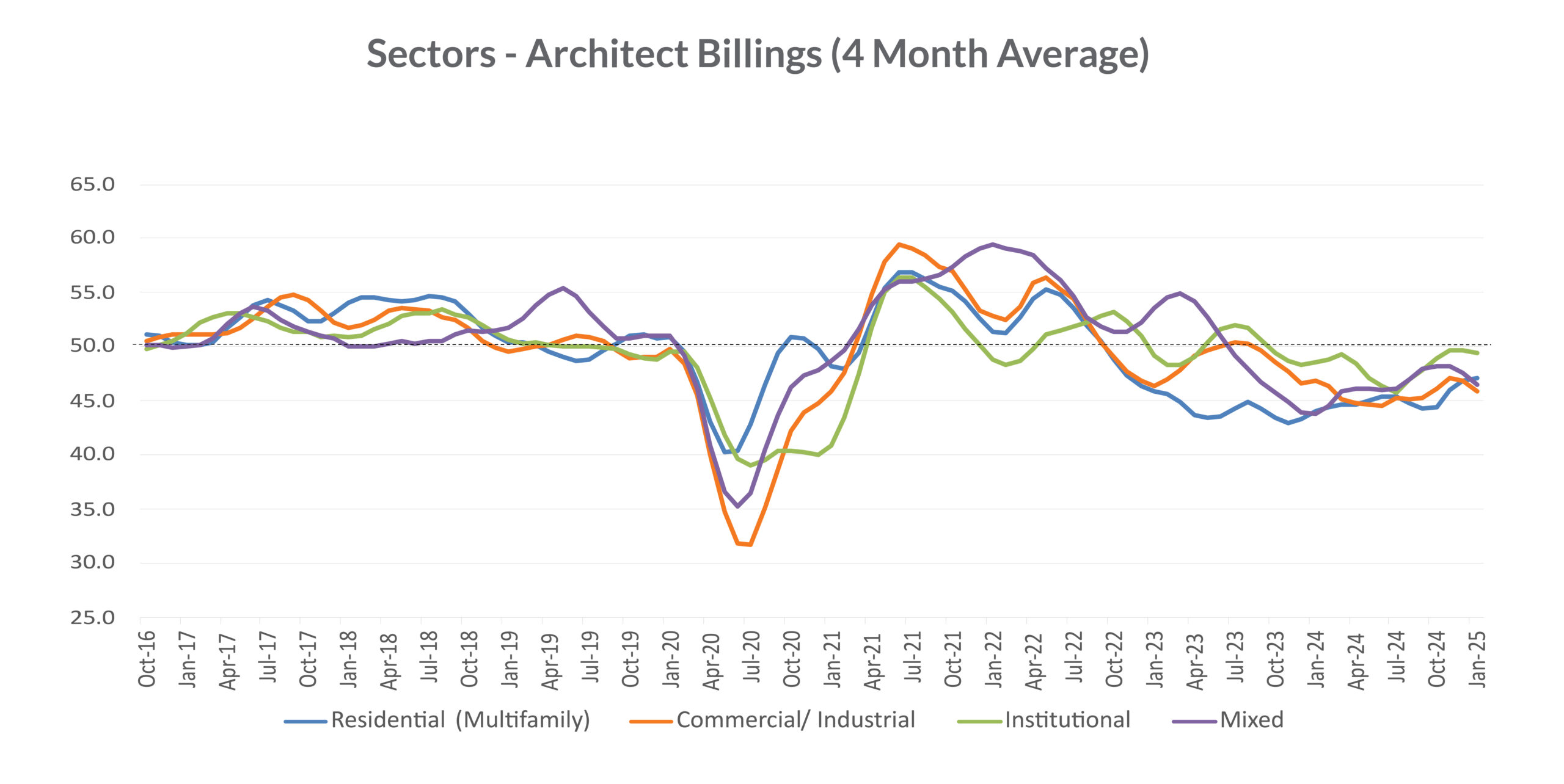

3. Architectural Billings Signal Continued Softness in Development

Source: The American Institute of Architects

Architectural billings remain below the 50.0 threshold, indicating an ongoing contraction in new project activity. While the commercial/industrial sector has shown marginal improvement, overall demand for architectural services remains tepid, reflecting developers’ reluctance to initiate new projects. Persistent concerns over construction costs, financing constraints, and economic uncertainty are prompting many developers to delay or scale back plans, particularly in sectors facing high vacancy rates or oversupply.

What this means for you:

Slower architectural activity suggests more limited future supply, creating opportunities for property owners and lenders. Investors should focus on increasing value through renovations, repositioning, and operational enhancements to maintain competitiveness. Reduced development could increase the scarcity value of well-located assets, particularly those in high-demand areas, thus potentially boosting long-term appreciation, rental growth, and collateral value.

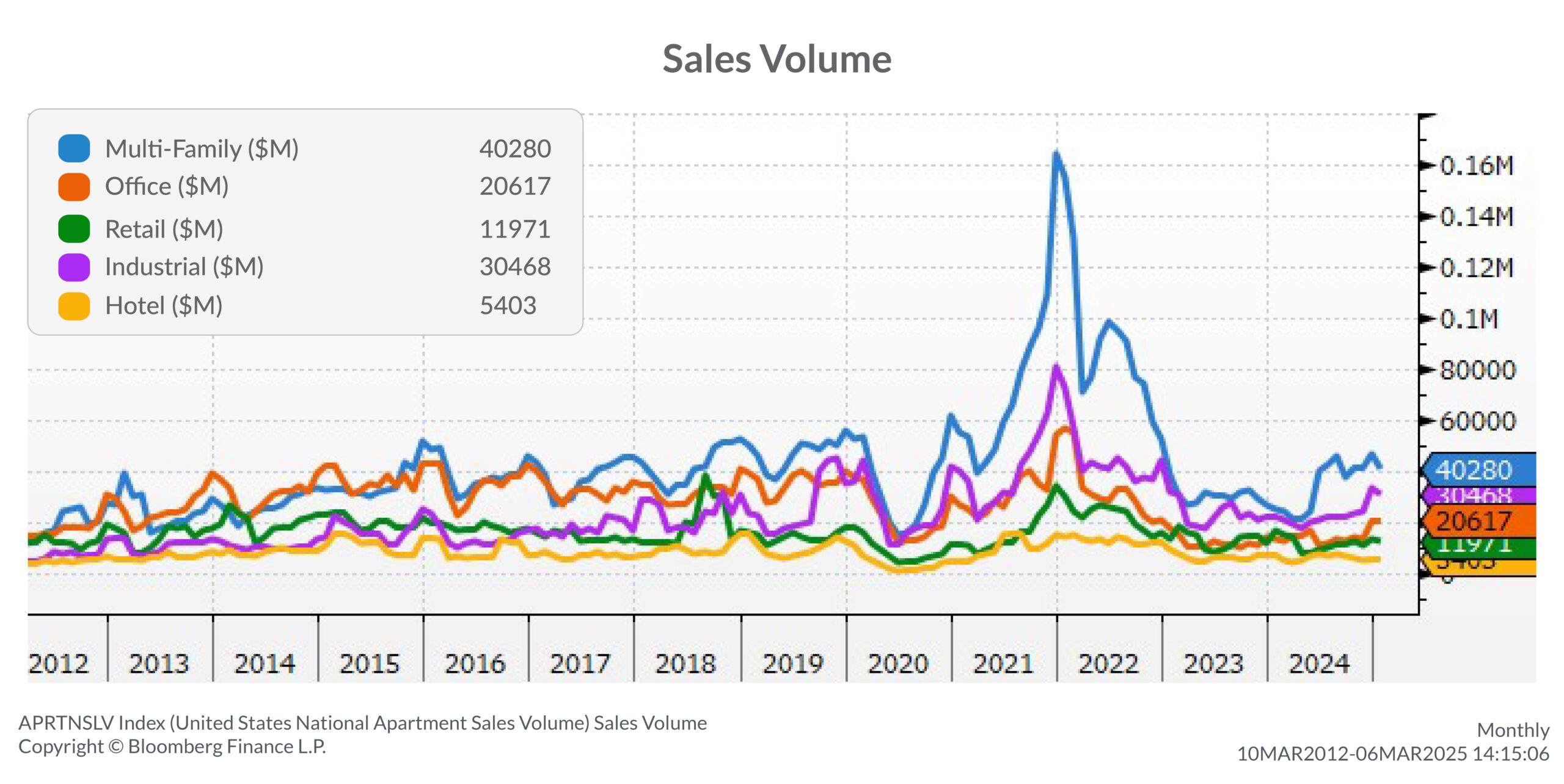

4. CRE Transaction Volumes Show Signs of Stabilization

Source: Bloomberg Finance L.P.

Following a steep decline in 2022-2023, transaction volumes in key asset classes are beginning to stabilize. Multifamily and industrial segments continue to drive most activity, reflecting their strong underlying demand and relative resilience. In contrast, office and hotel transactions remain subdued, hindered by ongoing structural challenges, shifting tenant preferences, and financing constraints. As capital markets adjust, pricing discovery is expected to remain a key factor in deal activity throughout 2025.

What this means for you:

Liquidity is gradually improving, particularly in resilient asset classes like multifamily and industrial. However, transaction activity remains selective, with investors focusing on high-quality properties and well-located assets. As pricing discovery continues, patience and disciplined capital deployment will be key. Investors should target assets with strong fundamentals, stable cash flows, and long-term demand drivers, while remaining prepared to act on opportunistic acquisitions as market conditions evolve.

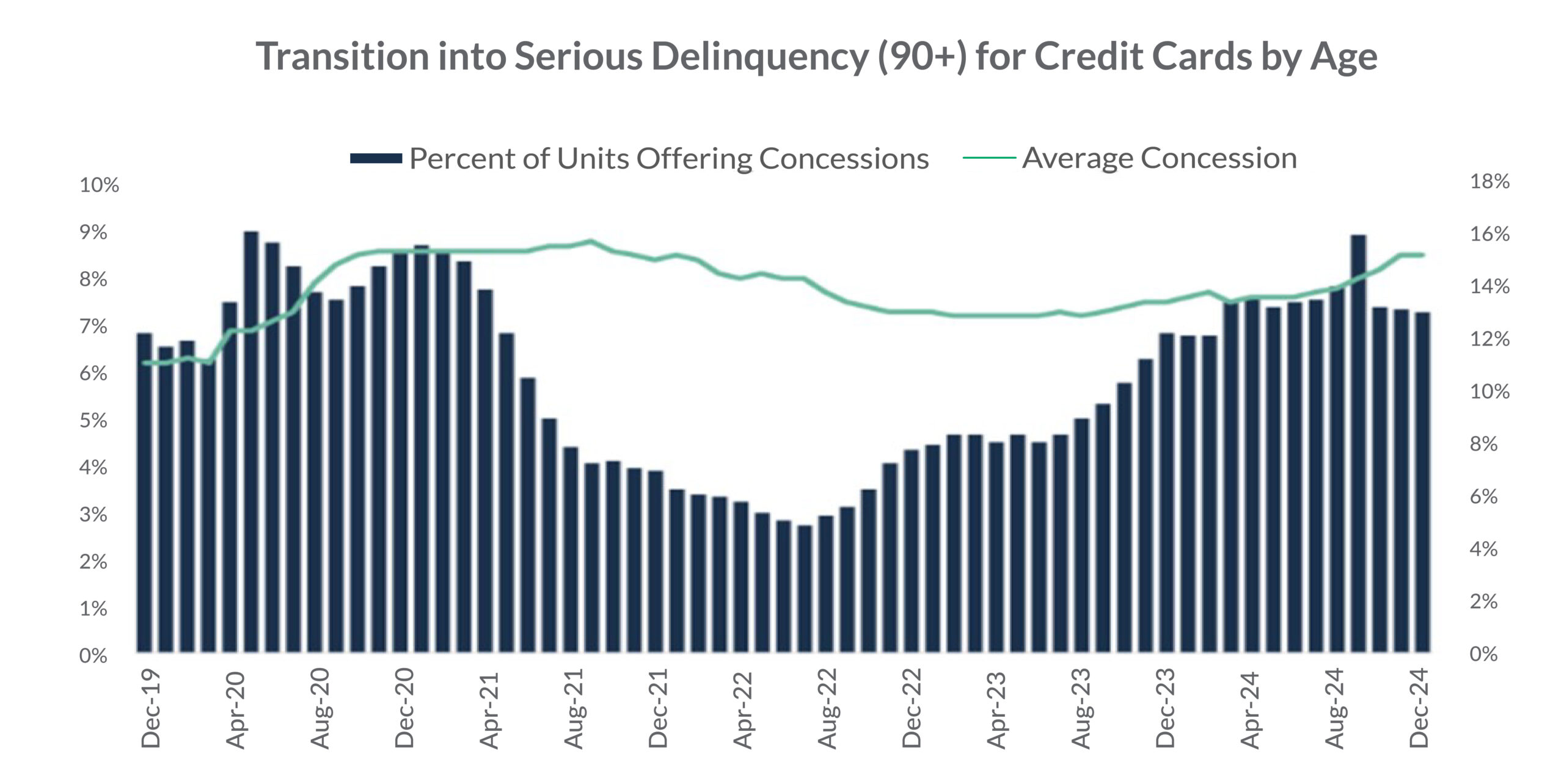

5. Multifamily Concessions Rise as New Supply Pressures Rents

Source: RealPage Market Analytics

The percentage of multifamily units offering concessions has risen sharply, reaching levels that were last seen in the early months of the pandemic. In response to increased competition from newly delivered properties, landlords in oversupplied markets are offering more aggressive incentives, such as multiple months of free rent, reduced security deposits, and waived fees. Average rent concessions now exceed 14% in select markets, with certain high-supply metro areas experiencing even deeper discounts as owners seek to maintain occupancy levels and cash flow amid heightened leasing challenges.

What this means for you:

Multifamily owners should focus on property differentiation by enhancing amenities, improving property management, and leveraging targeted leasing strategies to attract and retain tenants. Offering value-add services such as smart home technology, co-working spaces, or flexible lease terms can help maintain occupancy and pricing power. Strategic acquisitions of well-located, cash-flowing properties in constrained supply markets—or where asset owners have existing properties to leverage fixed costs—may offer strong long-term potential.

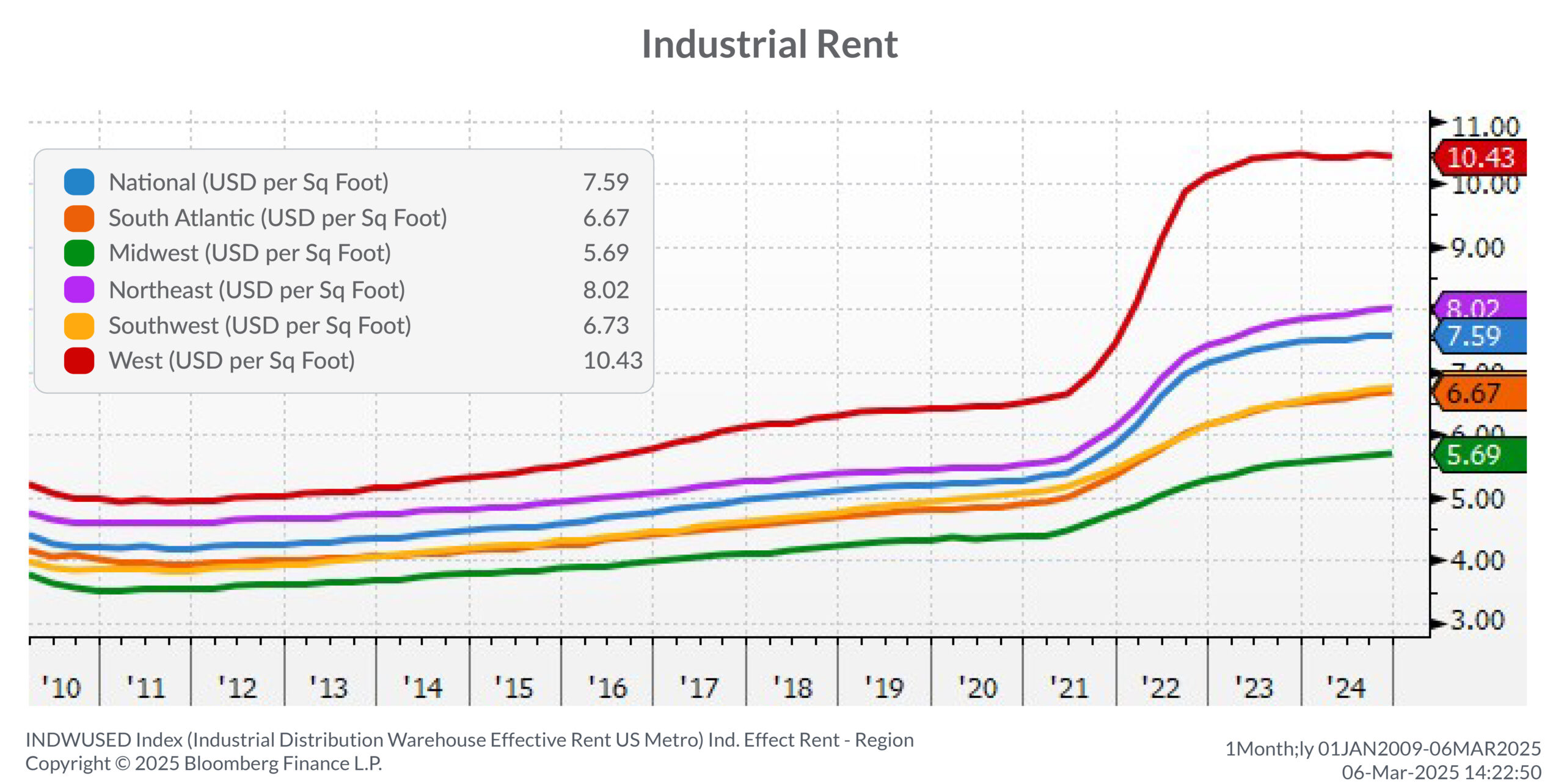

6. Industrial Rents Hold Near Record Highs, But Growth Moderates

Source: Bloomberg Finance L.P.

Industrial real estate remains a top-performing sector, with effective rents holding near historic highs, driven by sustained demand for logistics and warehousing. The West region continues to lead the nation in rent levels, fueled by supply chain resilience and infrastructure investments. However, rent growth has moderated as new supply enters the market, creating a more balanced dynamic between landlords and tenants. While fundamentals remain strong, regional variations in absorption and vacancy rates indicate that investors should be increasingly selective in targeting markets with persistent demand and supply constraints.

What this means for you:

Investors should prioritize regions with persistent supply constraints and strong logistics demand as these areas are likely to sustain rent growth and high occupancy rates. Additionally, focusing on properties with modern logistics capabilities, such as high-efficiency warehouses and strategically located distribution centers, can provide a competitive edge in an evolving industrial market. As supply and demand dynamics shift, investors should remain agile and evaluate opportunities to acquire assets in high-growth logistics hubs, while monitoring regional absorption and vacancy trends.

This commentary is brought to you by our advisors at Aprio.

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the publication date and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Certain investor qualifications may apply. Definitions for Qualified Purchaser, Qualified Client and Accredited Investor can be found from multiple sources online or in the SEC’s glossary found here https://www.sec.gov/education/glossary/jargon-z#Q