At a glance

- The main takeaway: The IRS officially released a new templated form for taxpayers to use when making a Section 83(b) election.

- Impact on your business: There are rare situations when making a Section 83(b) election would not make sense, this is a critical decision.

- Next steps: Aprio guide you through understanding the new Section 83(b) form and determine if an election is right for you.

Schedule a consultation

The full story:

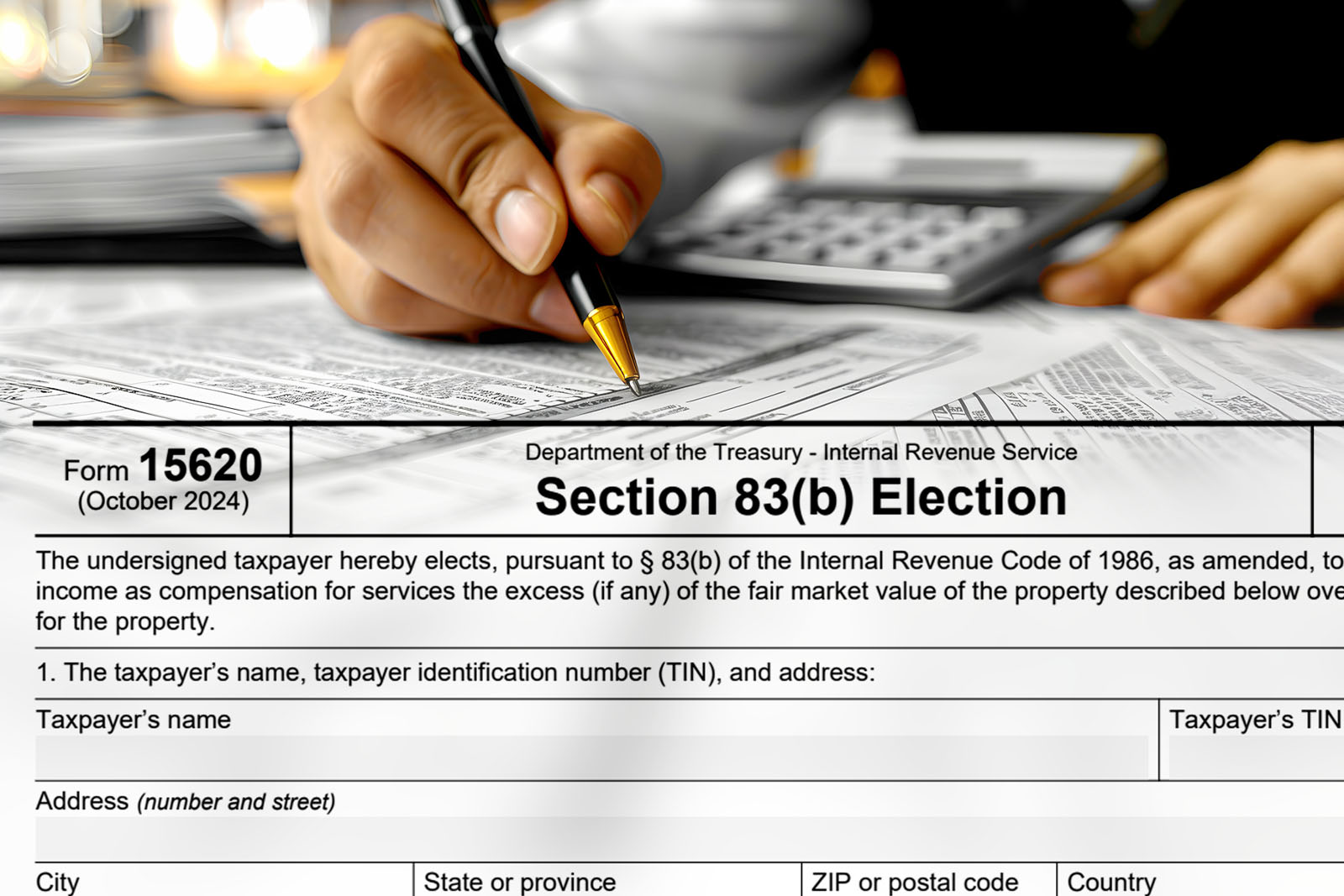

The IRS released major news on November 7, 2024. If you guessed the long-awaited templated IRS Section 83(b) form, then you’d be correct.

IRS Form 15620, commonly known as Section 83(b), is as straightforward as the historical election format we have spent decades preparing for clients. What has not changed, as a result of this new form, is who should file this election, when it’s due, and what information should be disclosed.

While many tax elections can be filed late, Section 83(b) elections cannot. The due date is 30 days from the date you receive/purchase the property/equity.

Types of transactions for an 83(b) election

There are three types of transactions in which taxpayers should consider making an 83(b) election:

- Receipt or purchase of restricted stock

- Early exercise of qualified and non-qualified stock options

- Receipt or purchase of partnership/membership interest

Common Section 83(b) election misconceptions

It’s important to note that there are rare situations where its best for taxpayers to not make an 83(b) election. One of the biggest misunderstandings is that the decision to make a Section 83(b) election is only of interest to the taxpayer who receives or purchases the equity instrument. While this is technically correct, the company has extremely specific tax reporting obligations, which differ dramatically if a recipient does or does not make a timely election. The taxpayer and/or recipient must provide a copy of the Section 83(b) election they file with the company who issued the equity subject to the election.

The bottom line

While the IRS created a new templated Section 83(b) form, it’s not an easy button for taxpayers. The difficult part of this process is understanding whether an election should or should not be filed.

Aprio can navigate you through the journey of why, when, and how to make a Section 83(b) election.

Schedule a consultation