COVID-19 Puts the Squeeze on Transaction Multiples and Deal Volume

June 4, 2020

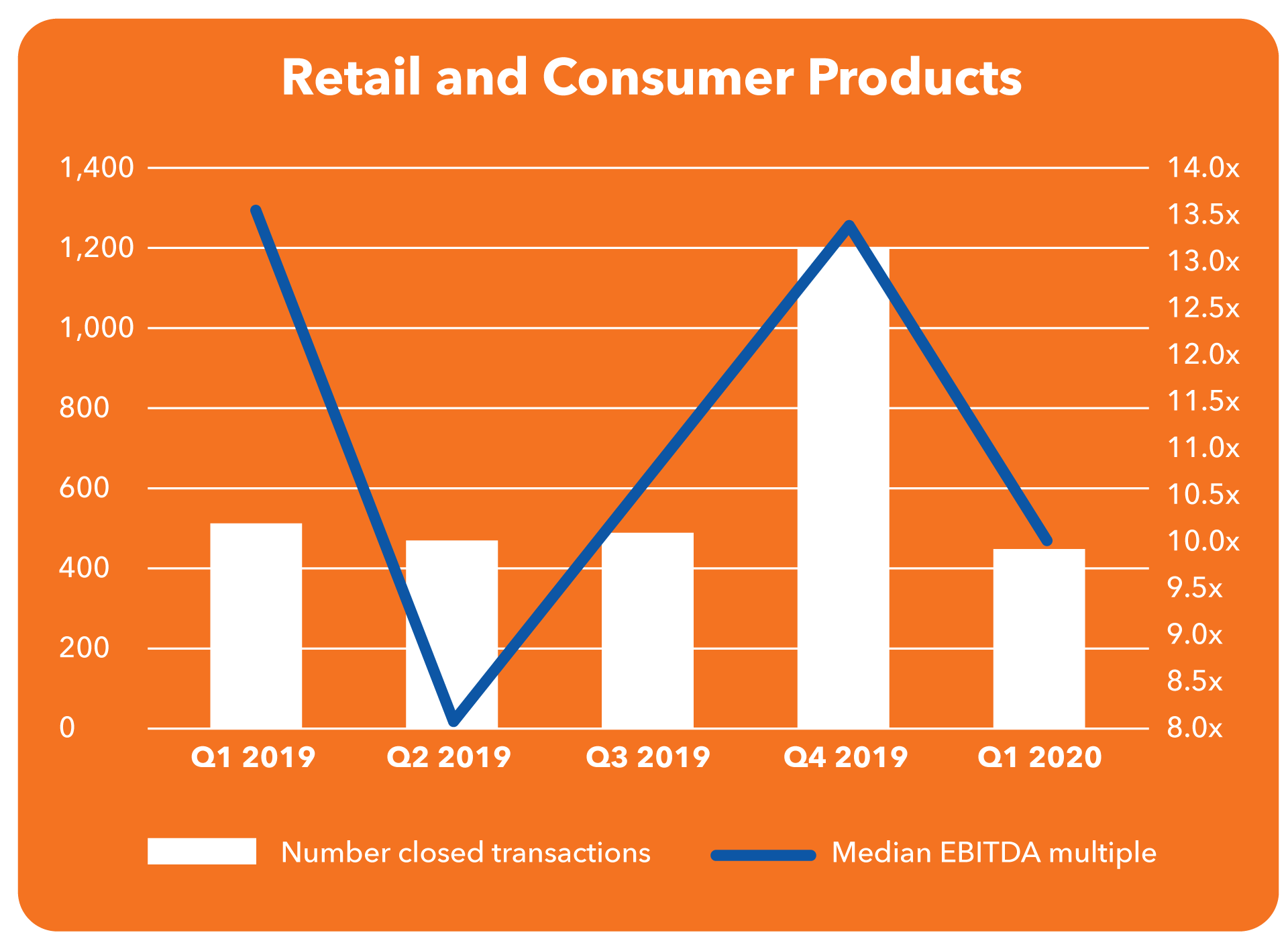

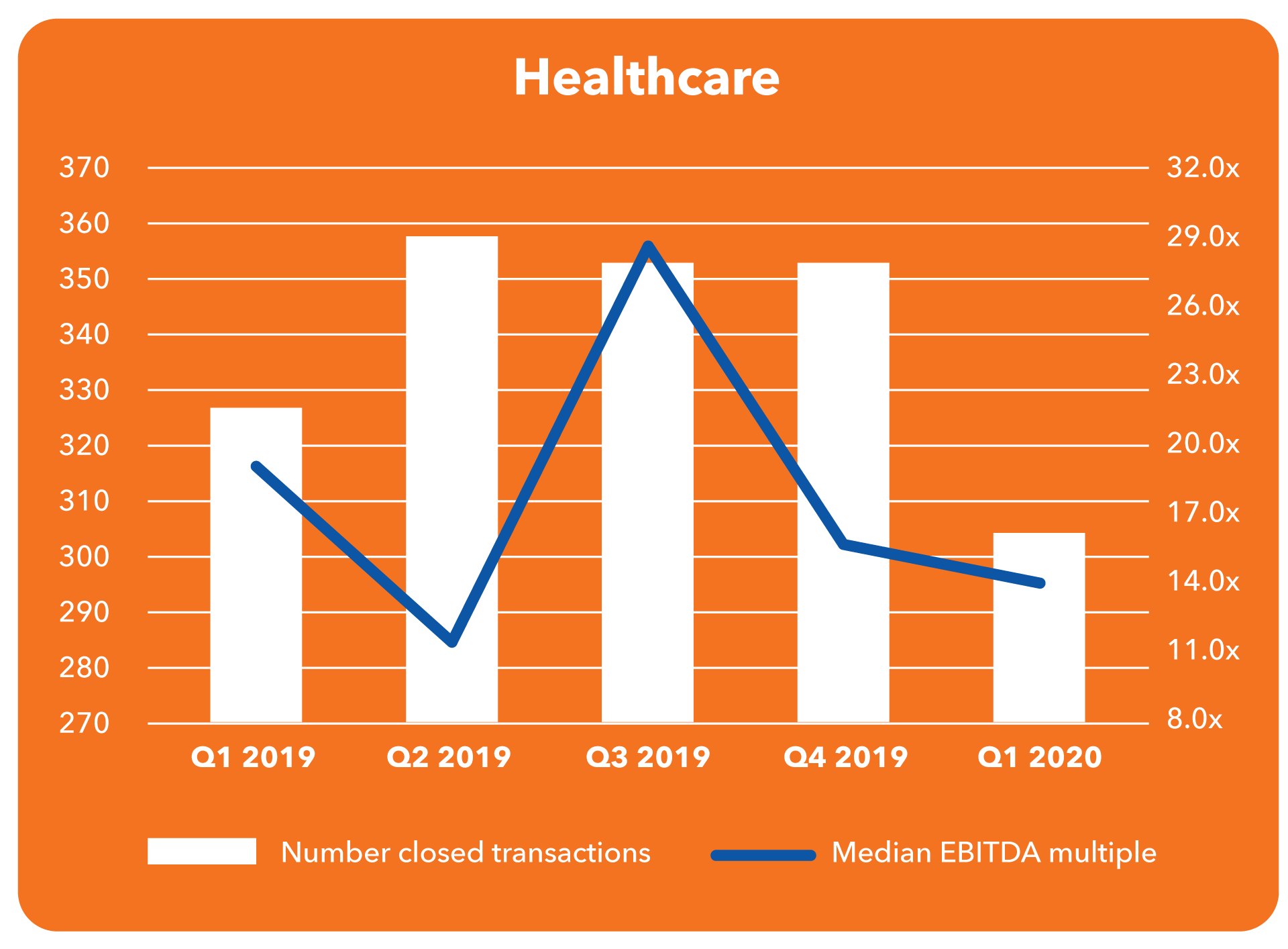

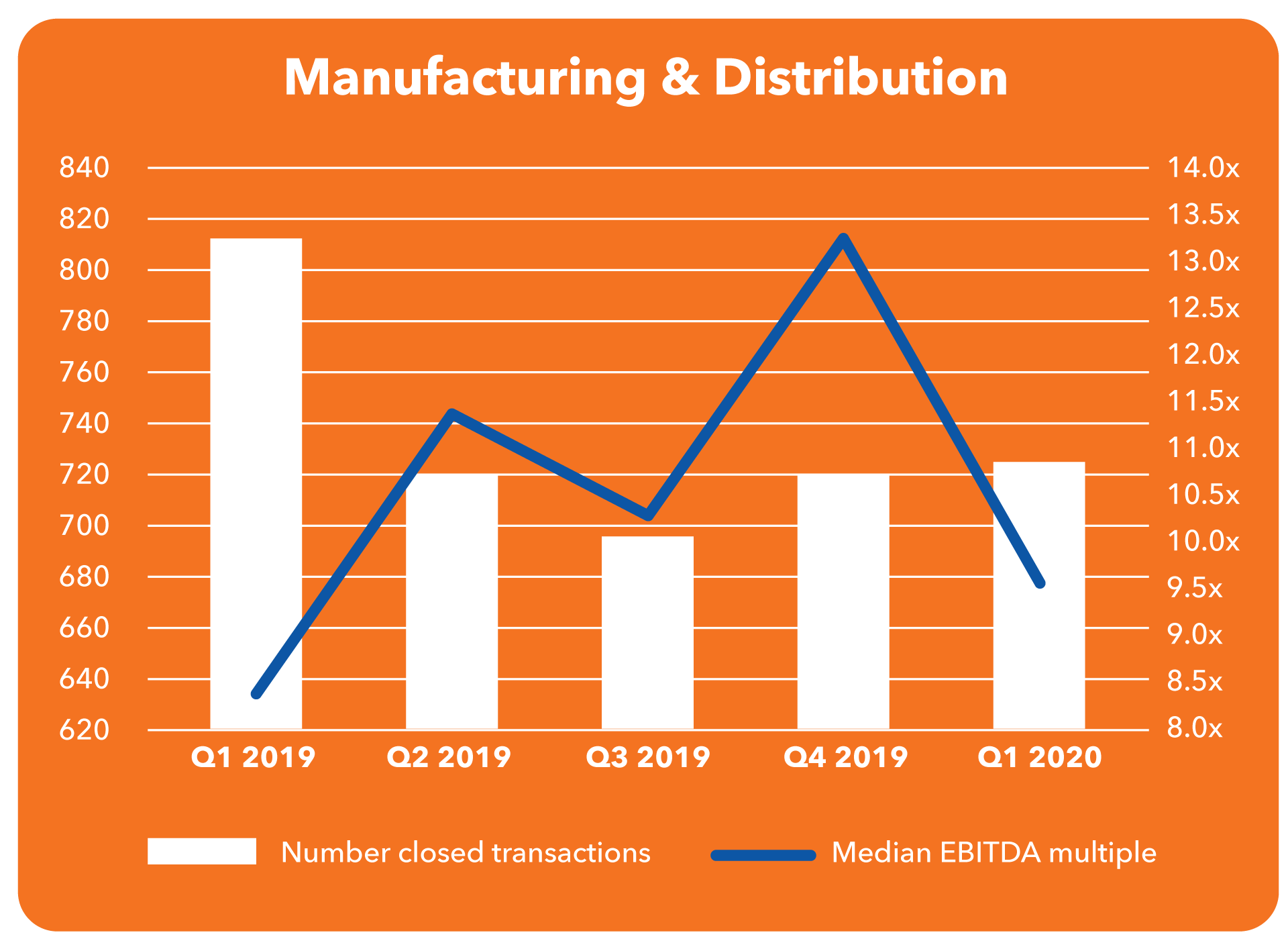

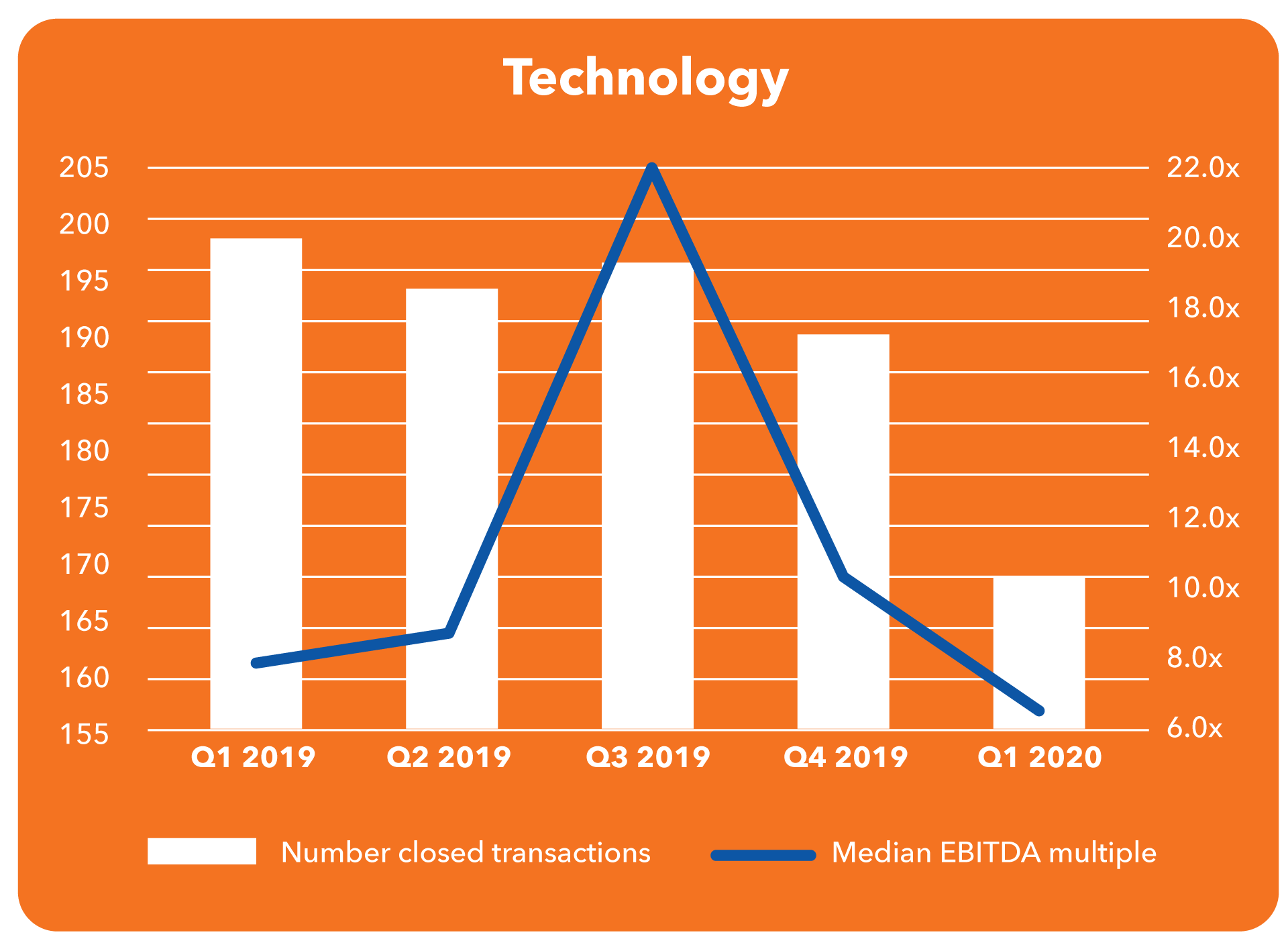

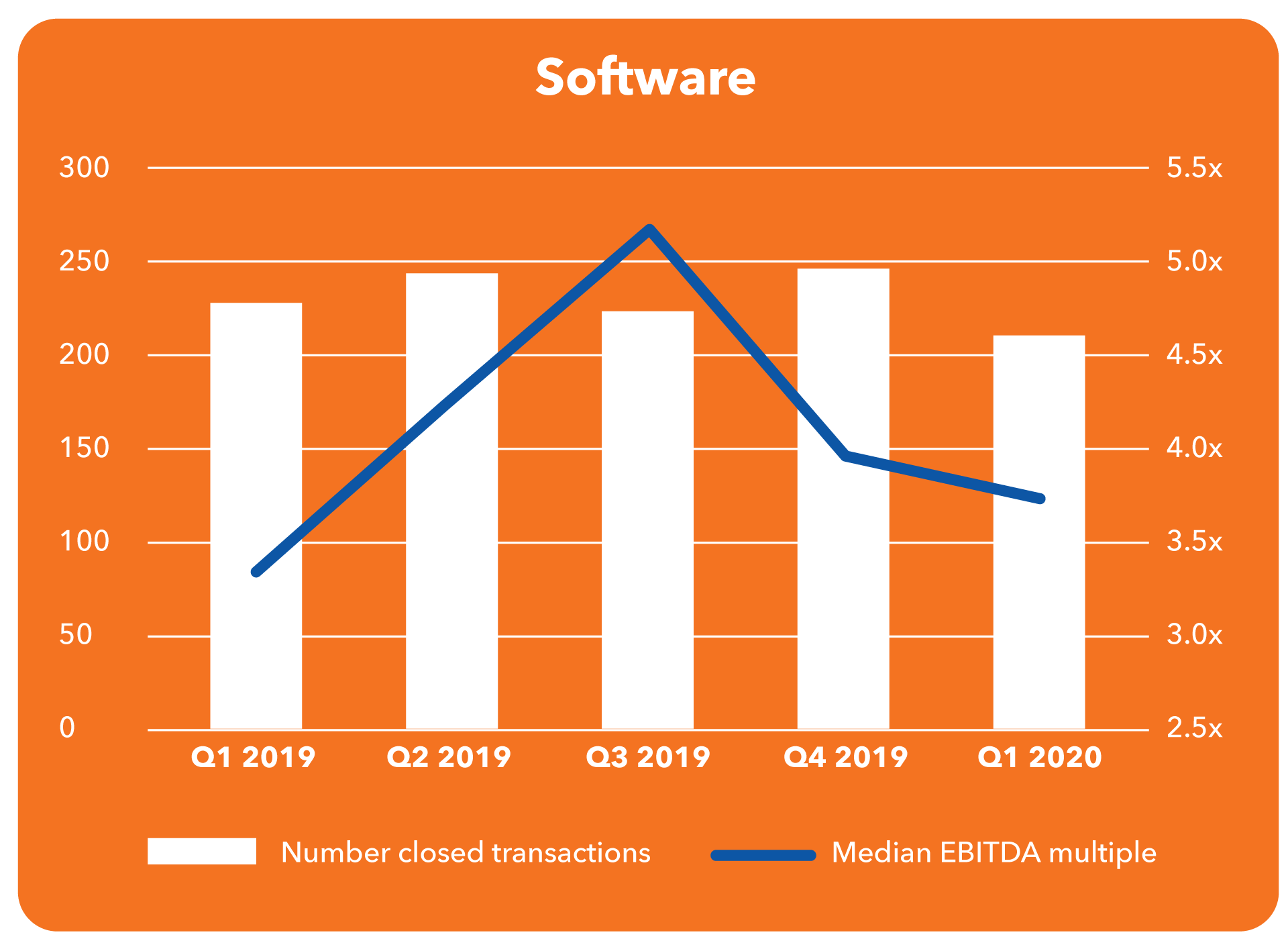

The Wall Street Journal ran a story on March 31, 2020, “Coronavirus Throws Deal Making Into Disarray” with the punch line that deal volume has started to dry up. As weekly deal volume, even in good times, can be volatile, we wanted to look at how U.S. deal volume and multiples held up in some of Aprio’s industry groups in Q1 2020 as compared to each of the fiscal quarters in 2019.

Based on data from CapitalIQ[1], we are seeing not only a drop in deal volume in these industry sectors (based on the number of closed deals in a given quarter), but also a sharp pull back in median deal multiples. In addition, with 2020 being a leap year, March had 34% of the days in Q1 2020, but only 20% of the deals closed.

With much of the U.S. just starting to adjust to COVID-19 remote work and shelter in place orders as March progressed, does the worrisome trend we are seeing in March have further implications of a much slower transaction market during Q2 2020, as well as the rest of the year? Will sectors such as healthcare and technology, which are thought to be at the front end of the recovery see an uptick in deal volume as the year progresses?

Aprio industry groups deal activity

Key questions to be answered…

As we monitor credit markets, with banks being more cautious to fund transactions, which may be offset by all the liquidity that will come to market with government incentives, we are curious to see how the transaction markets shape up for the rest of the year.

- Will deals funded with lower leverage or stock support keep middle market transactions moving forward?

- Will family offices or strategic buyers with longer holding periods feel comfortable investing and riding out near-term dislocation?

- Finally, how do you source and move forward a transaction with buyers, sellers, accountants, bankers and attorneys all working from home?

And while the equity markets entered bear market territory, defined as a drop of more than 20% from a high point, both the Dow and S&P technically pulled out of bear territory the second week of April. As I write this article, both indices are up approximately 2%. All this volatility leads us to believe there is still a lot of uncertainty as to the economic impact, both short and long term, of COVID-19. In fact, Barrons’ ran an article on this on April 8, 2020, “The Stock Market Is Back in a Bull Market. That Doesn’t Mean the Bear Is Over.”

We will continue to track these numbers and post monthly updates to track the market in a more real time basis. Our goal is to share insights that can start providing better answers to these questions posed in this article. Stay tuned.

[1] Not all transactions had enough information for CapitalIQ to calculate a multiple. As an example, of the approximately 350 healthcare transactions in Q3 2019, only two had meaningful multiples, both of which were in a similar range and as such, are presented in healthcare graph.

Stay informed with Aprio.

Get industry news and leading insights delivered straight to your inbox.