The Pulse on the Economy and Capital Markets: April 19–23, 2021

April 27, 2021

Executive Summary

-

- Mixed Signals: Earnings of companies started stronger than expected last week, though markets did not react to the news.

- Full Steam Ahead? Economic data shows the economy is accelerating, yet shortages are popping up across a variety of products, which could slow down some of this momentum. Meanwhile, savvy companies are starting to order inventories further out than they have traditionally.

- The Scarcity Challenge: We continue to see stretched supply chains as a potential issue for many sectors, including rail and trucking.

In the Markets

First-quarter earnings season has started strong, with ~25% of S&P 500 companies reporting earnings. Eighty-six percent of reporting companies have beat analysts’ estimates, the highest level in years. Here are a few key data points:

- Compared to Q1 2020, companies have grown in revenue 7% and in earnings 34%, ahead of expectations.

- The financial services and materials sectors have had the strongest year-over-year growth to date, both of which reflect the rebounding economy and consumers’ strong balance sheets.

With 176 S&P 500 companies reporting earnings, this week is a big one for earnings announcements, especially for the industrials and healthcare sectors.

Last week, the market took a breather after a strong start to the month. Markets are concerned about rising COVID-19 cases internationally — notably in India — and how that might impact expected GDP growth and travel.

This more conservative posture was reflected in real estate and healthcare as the two top-performing sectors last week; both share recurring revenues so they are considered more defensive by investors.

In the Economy

The economic news continues to come in very positive. Last week, we received the Conference Board’s monthly Leading Economic Indicators Index, which is a composite of 10 economic components that signal the direction of the economy.

One of the Index’s most notable points: March was at its highest level in over a decade (excluding the initial COVID-19 rebound from shut-downs).

High-frequency data across the economy continues broad-based improvement — almost everything is green, with week-to-week and month-over-month improvements. One of the areas that has shown continued strength is lodging and rail car traffic, which we highlight below.

Stretched supply chains

Supply chains continue to be stretched, a common issue in the early stages of a rebound, and scarcity will ultimately lead to increased asset value.

The current stretch is made more challenging by requisite social distancing precautions before we achieve herd immunity from COVID-19. Countries that reach herd immunity first will have an economic competitive advantage for a period because they will have greater production and service capacity.

“Blue Horseshoe Loves Anacott Steel”

In a throwback to the bidding wars of the 1980s for companies with valuable tangible assets, a new bidder emerged for the railroad, Kansas City Southern (KSU).

Canadian National, Canada’s largest railroad, offered $30 billion for KSU, topping smaller rival, Canadian Pacific (CP)’s, $25 billion bid. Here are a few points to consider:

- As we noted when CP’s offer was announced, KSU has highly sought-after railways deep into Mexico, tied into the country’s industrial footprint.

- Integrating the railroads from Canada to Mexico can reap huge savings and efficiencies.

Railroads are the backbone of shipping commodities. This week, The Home Depot’s chief financial officer (CFO) noted why this capability will be so important over the next decade:

“I’d say the things that we’re watching are the fact that there’s a housing shortage today. It’s unlike any we’ve seen post-World War II. The question will be the persistence of that housing shortage. The Wall Street Journal, and I think it was Freddie Mac, this morning came out with a number that showed that, in essence, we have a housing deficit of about 3.8 million units just in the United States. So, that will most likely provide support for home price appreciation as demand outstrips supply. We saw the household formation dynamic in 2020 grow at a different trajectory than we had in many years. So, we’ve been underbuilt for about 10 years. We’ve been underbuilding for 10 years.” —Richard McPhail, CFO of The Home Depot (HD)

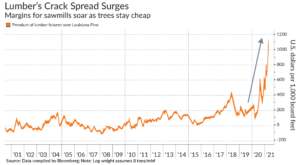

Home-building requires lumber, and lumber is shipped on rails — especially out of Canada and from the Southern U.S. Lumber prices have soared (as anyone who recently has been to The Home Depot or Lowe’s will attest).

It’s the lumber mills, not the tree owners, that are profiting. In fact, the trees themselves are at their lowest level in a decade, according to this Bloomberg article (link).

So, why are the mills coming out on top? The reason is scarcity (again) — sawmills are capacity-constrained due to fewer workers and reduced capacity from years of weak prices.

Scarcity is in abundance these days

Scarcity is rearing its head in another corner of transportation: trucking.

In a recent earnings call, the chief executive officer (CEO) of J.B. Hunt, a national trucking company, noted:

“While we have faced driver hiring issues at varying degrees of difficulty during previous tightening cycles, we see the current pressure being meaningfully more pronounced and likely prolonged.” — John Roberts, CEO of J.B. Hunt (JBHT)

Companies are starting to address this, but they must be proactive. Fastenal, a large and growing industrial distributor that touches thousands of businesses across various sizes, had its CFO recently say:

“Historically, our supply chain team might be pinging branches with reorder points that are 90 days out, 100 days out, 110 days out. What our supply chain teams are doing, we are going out even further. We are going out into August and September, and we are pinging folks and saying, ‘Hey, we might want to order this now.’” — Holden Lewis, CFO of Fastenal (FAST)

Scarcity is hitting auto production hard, too, as semiconductor production is lagging (link). As a result, Ford and General Motors are shutting plants, such as the one that builds the highly profitable F-150 pick-up. The industry itself has lost production of 1.4 million vehicles and $61 billion in revenue.

A Few Stories That Caught My Eye

- Get a closer look at the home and home-builder shortage we discussed above (link).

- The growing microchip shortage is also dragging down the auto industry, according to AutoNation CEO Mike Jackson (link).

- Nike lost two big stars last week: Gold medalist Simone Biles for Athleta (link) and the late Kobe Bryant (link), whose shoes were worn by 20% of NBA players last year.

Disclosures

Investment advisory services are offered by Aprio Wealth Management, LLC, a Securities and Exchange Commission Registered Investment Advisor. Opinions expressed are as of the current date (April 27, 2021) and subject to change without notice. Aprio Wealth Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment.

This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Aprio Wealth Management, LLC’s investment advisory services.

Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Any securities mentioned in this commentary are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful.

Securities offered through Purshe Kaplan Sterling Investments. Member FINRA/SIPC. Investment Advisory Services offered through Aprio Wealth Management, LLC, a registered investment advisor. Aprio Wealth Management, LLC and the Aprio Group of Companies are not affiliated with Purshe Kaplan Sterling Investments.

Recent Articles

About the Author

Simeon Wallis

Simeon is the Chief Investment Officer of Aprio Wealth Management and the Director of Aprio Family Office. He brings to his role two decades of professional investing experience in publicly traded and privately held companies as well as senior-level operating and strategy consulting experience.

(470) 236-0403

Stay informed with Aprio.

Get industry news and leading insights delivered straight to your inbox.