After a year of uneven growth, the manufacturing sector is showing signs of stabilization. Production is once again expanding, factory construction remains elevated, and new orders are beginning to outpace inventories — early signals of a potential rebound. Despite input costs and shifting trade dynamics, margins are holding steady. For manufacturers and distributors, the message this quarter is cautious optimism: seize the moment by prioritizing efficiency, controlling costs, and preparing for a gradual but steady recovery.

1. Signs of Stabilization in Manufacturing

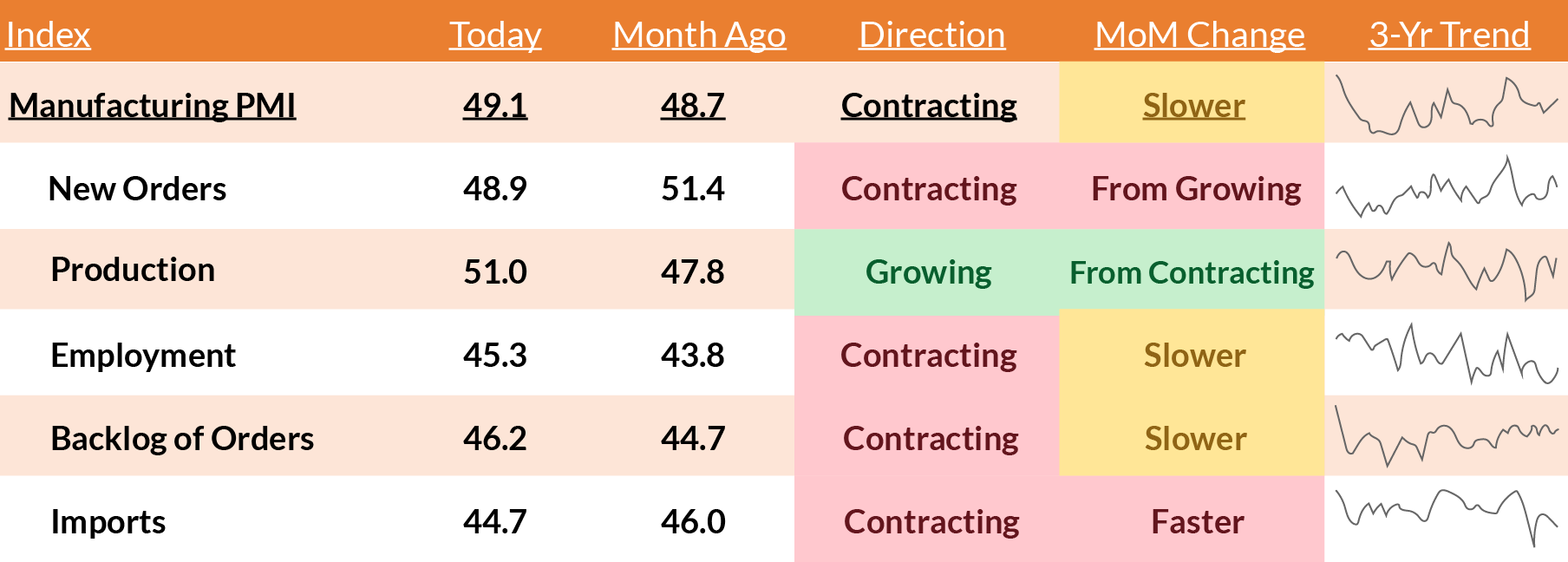

Source: Institute of Supply Management (ISM)

The Manufacturing PMI climbed to 49.1, marking its highest reading in six months and edging up from 48.7 last month. Production ticked into expansion territory at 51.0 for the first time since spring, signaling renewed momentum on the shop floor. While New Orders (48.9) and Employment (45.3) remained weak, both showed modest improvement. Imports are decelerating and backlogs are reducing at a gentler pace.

What this means for you: The sector may not be in full recovery yet, but the pace of the slowdown is easing. Factories are operating leaner, producing more with fewer employees, a testament to their history of resilience and adaptation. This is a critical time for business leaders to prioritize cash management, invest in productivity tools, and embrace automation. Staying agile will help capture growth opportunities when the increase in demand eventually picks up.

2. New Orders are Once Again Outpacing Inventories

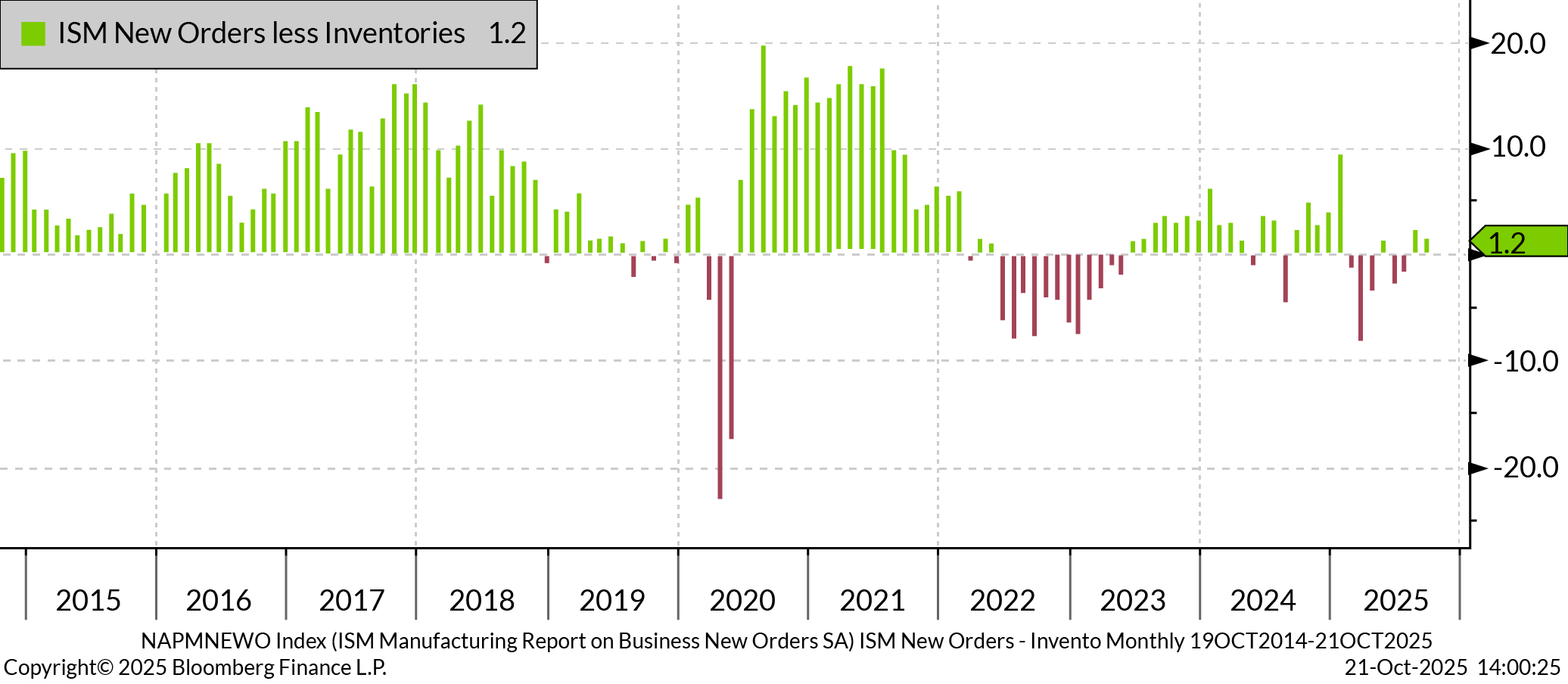

Source: Bloomberg Finance, LP

For the first time in over a year, the ISM “New Orders less Inventories” index has posted two consecutive months of positive readings. This improvement signals a subtle shift that new orders are now growing slightly faster than inventory levels, a pattern that has historically been a leading indicator of broader manufacturing recoveries by several months.

What this means for you: This shift is quiet but important. It sets the stage for excess inventory to clear up, and production to meet rising demand. Manufacturers should keep forecasts short-cycle but also begin to plan for selective restocking in faster-moving product lines. If sales continue to stabilize, 2026 could mark the start of a gradual expansion.

3. Navigating Mixed Signals from Input Costs

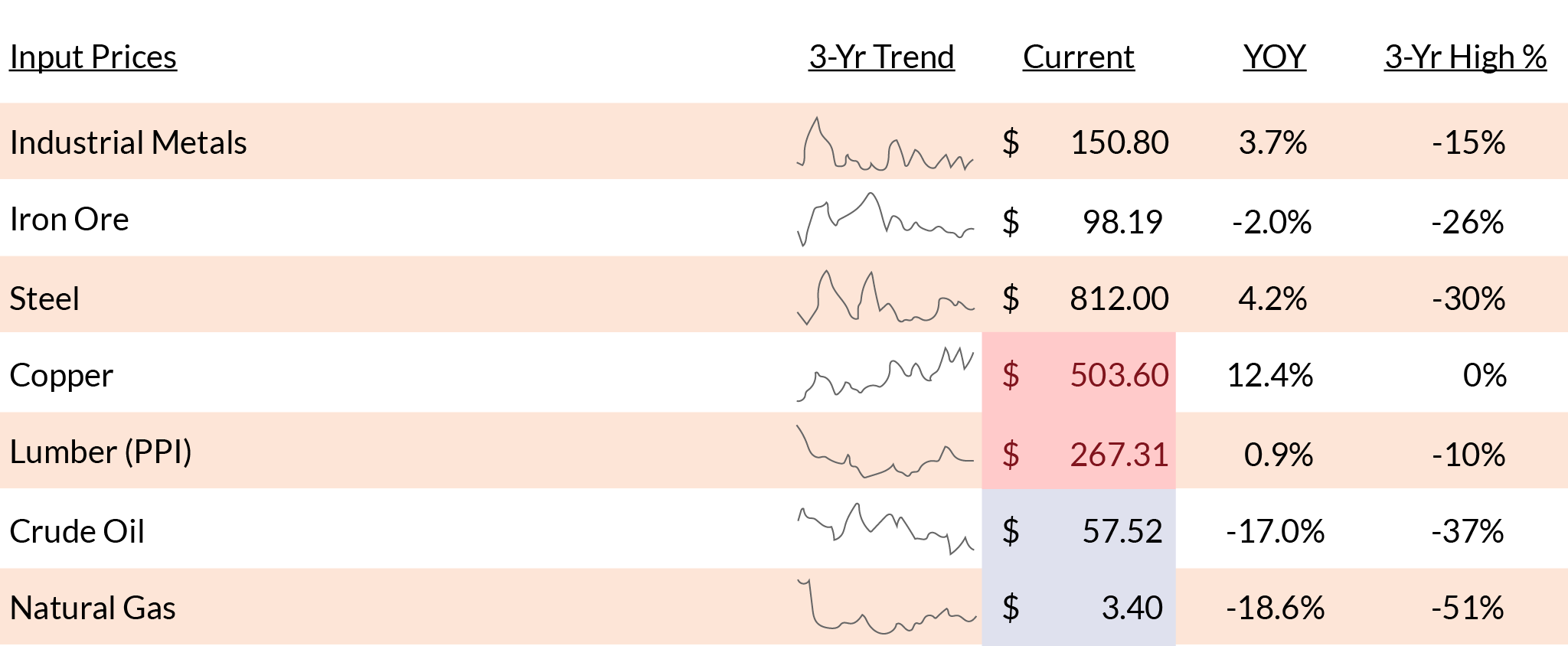

Source: Bloomberg Finance, LP

Commodity prices are sending mixed signals. Steel prices have climbed 4.2% year-over-year, and copper reached a historic high, driven by the anticipation of future demand from buildouts for AI, electrification, and re-shoring globally. In contrast, crude oil has declined more than 15%, reflecting weaker demand and robust supply as global growth slows and international production ramps up.

What this means for you: Material inflation hasn’t disappeared — it’s simply more selective. Manufacturers using steel and copper may face margin pressure, while those with energy-heavy production may benefit from the lower oil and gas costs. This divergence underscores the need for more granular cost planning strategies, such as hedging key inputs and locking in favorable energy contracts while volatility remains muted.

4. Factory Construction Remains Strong, but Pace is Easing

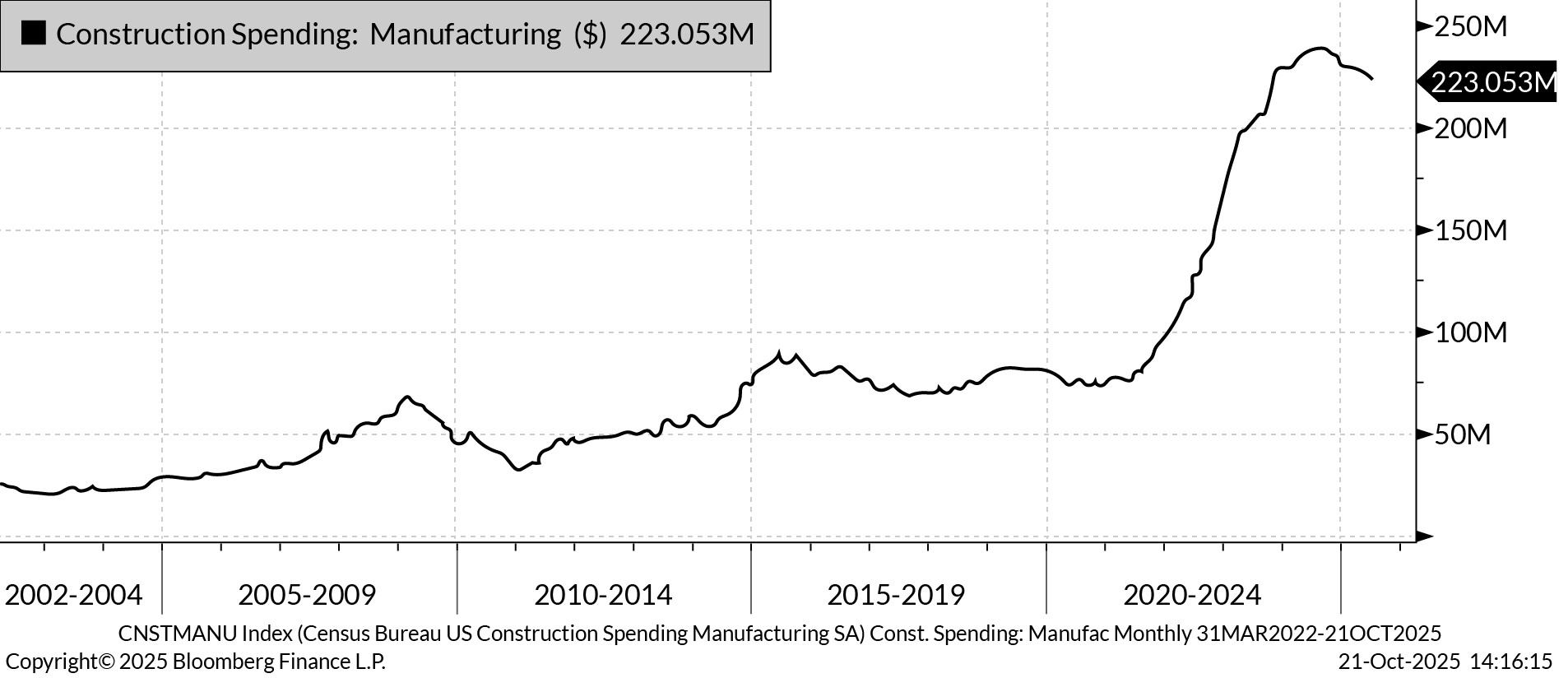

Source: Bloomberg Finance, LP

Spending on the construction of manufacturing facilities sits at $223 billion, still near record levels but easing from its recent highs. The surge, driven by reshoring, clean energy, and EV-related investment, is now leveling off as projects move from build-out to production.

What this means for you: The building boom is maturing and likely decelerating. Companies are focusing more on optimizing and operating new facilities over construction. Those considering expansion may benefit from competition for resources, even as borrowing costs may remain elevated, potentially opening opportunities to capture additional market share.

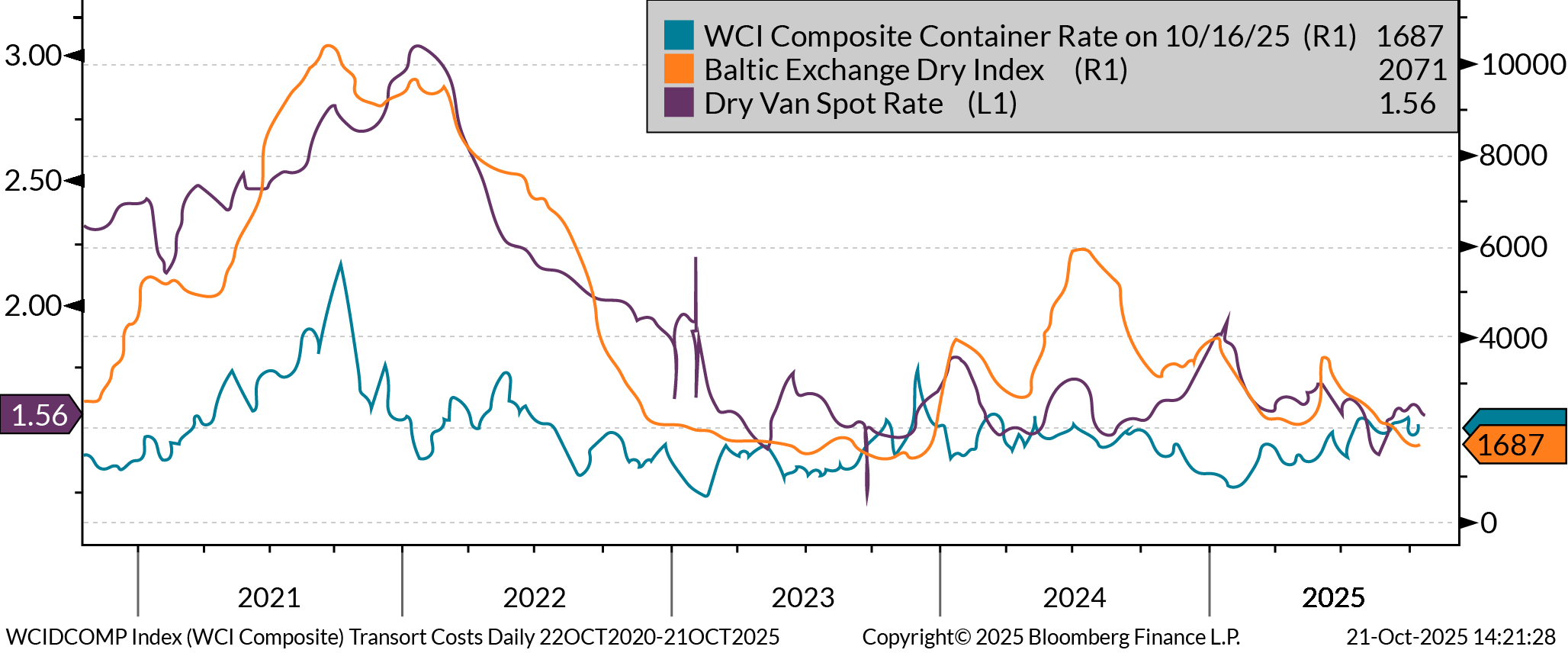

5. Freight Rate Divergence Reflects Uneven Demand

Source: Bloomberg Finance, LP

Freight markets are moving in different directions. The WCI Composite Container Rate has dipped from its mid-year highs, reflecting softer demand for goods shipped from Asia, potentially due to tariffs. Meanwhile, the Baltic Exchange Dry Index has climbed, signaling stronger global demand for bulk raw materials, such as iron ore and coal. The Dry-Van Spot Rate remains above pre-pandemic levels but is off its 2025 highs as domestic freight volumes stabilize.

What this means for you: Transportation costs mirror the economy’s mixed signals. Lower container rates reduce import costs, while rising bulk rates suggest steady global industrial activity in key commodities. For most manufacturers, this means importing materials could become cheaper even as export logistics slightly tighten. With domestic distribution holding steady, manufacturers should balance overseas sourcing with regional suppliers to manage costs and reduce exposure to global freight volatility. Diversifying logistics partners may help mitigate further volatility.

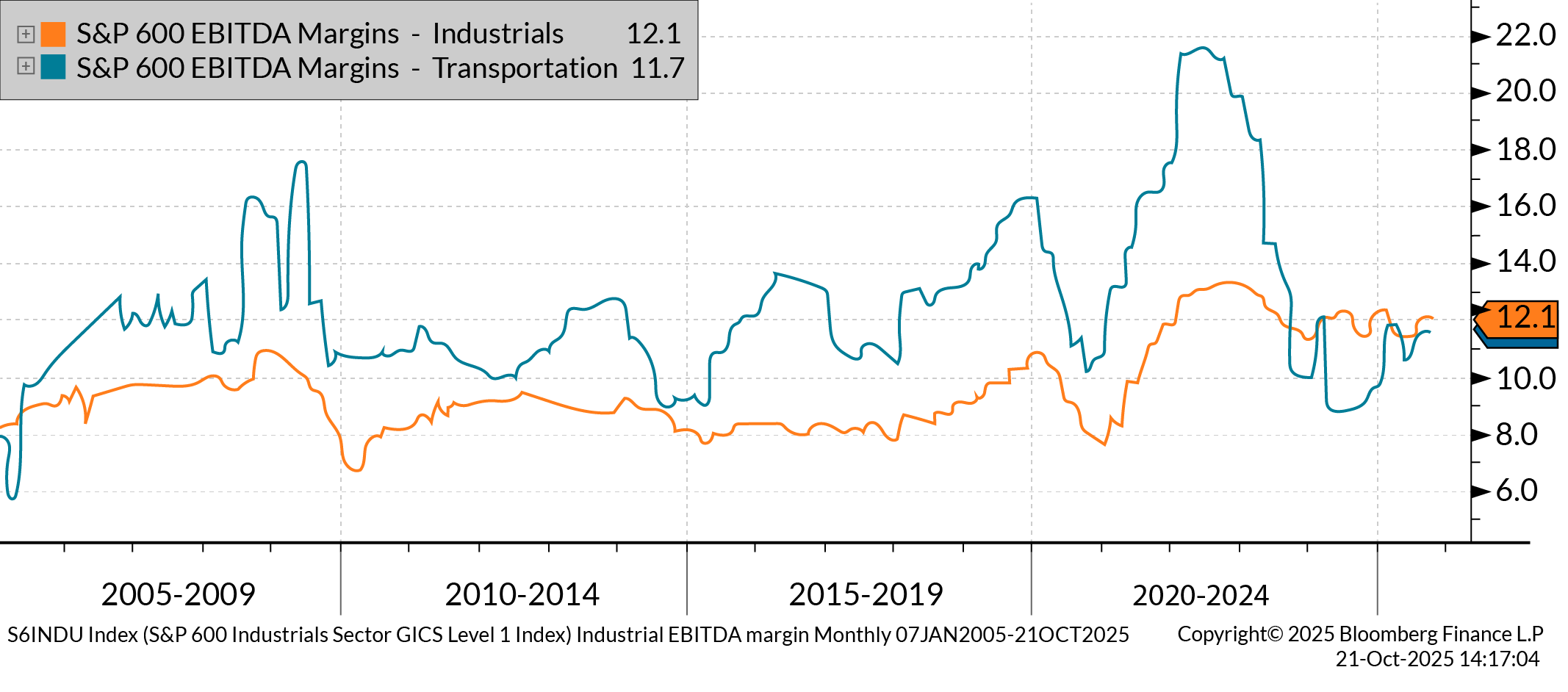

6. Margins Hold Steady Amid Cost Pressures

Source: Bloomberg Finance, LP

EBITDA margins for S&P 600 Industrials (12.1%) and Transportation (11.7%) remain stable over the past quarter. Both sectors are navigating the economic environment through disciplined cost management as they wait for margins to expand once demand sustainably grows.

What this means for you: Stability beats contraction — but staying profitable will require vigilance. With pricing power fading and costs diverging by input category, manufacturers need to focus on operational efficiency, disciplined pricing, and automation payback analysis. Every basis point of margin counts as the industry navigates 2026’s uncertain policy and trade environment.

This commentary is brought to you by Aprio advisors. If you have any questions, connect with our team today.