The Fundamentals – Pulse on the Economy and Capital Markets: 8/31/20 – 9/4/20

September 8, 2020

Executive Summary

Ahead of the holiday weekend, the employment and manufacturing numbers showed the rebound continues, though the headline employment numbers mask weakness related to Pandemic Unemployment Assistance (PUA) filings. The market, which had been strong through August, took a breather, led by the large tech companies which had surged throughout the year.

The Markets

The stock market’s decline, notably in the large cap technology companies that led the strong rebound over the last few months, captured headlines. In fairness, the selloff in the Nasdaq and S&P 500 returned to the levels of two weeks ago. The “risk off” mentality can be seen in the price of oil, which declined 7% for the week.

The top performing sector of the S&P 500 was Materials, which has been strong all quarter. The next two in line – Utilities and Financials – both of which have been out of favor and are strong dividend payers.

We saw investors shedding risk in the bond market too, as the spreads of high yield bonds widened (a sign that investors want to be paid more for their risks relative to risk-free U.S. government bonds).

The Economic News

This week marked strong August economic data from the manufacturing sector (which we will focus on), improving retail sales and better than expected employment figures. Although not without some concerns when we peel back the onion.

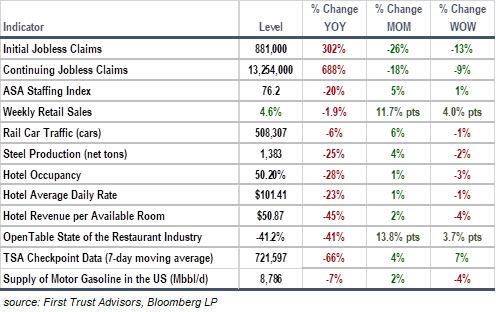

High Frequency Data

The New York Fed’s Weekly Economic Activity index continues to show improvements.

Focusing on monthly data shows the economy continues to rebound, with strong improvements in industrial activities (Rail Car traffic, Steel production) and increases in aspects of consumer lifestyles such as dining at restaurants and air travel. Hotels continue to lag the recovery (note: week-to-week comparisons are impacted by the Labor Day holiday).

The headline employment numbers were strong:

- Unemployment Rate was 8.4%, better than expected 9.8% and down from July’s 2%.

- Weekly initial unemployment claims continued their decline down to 880k from 1m last week.

- Continuing unemployment claims declined to 13.3m from 14.5m last week.

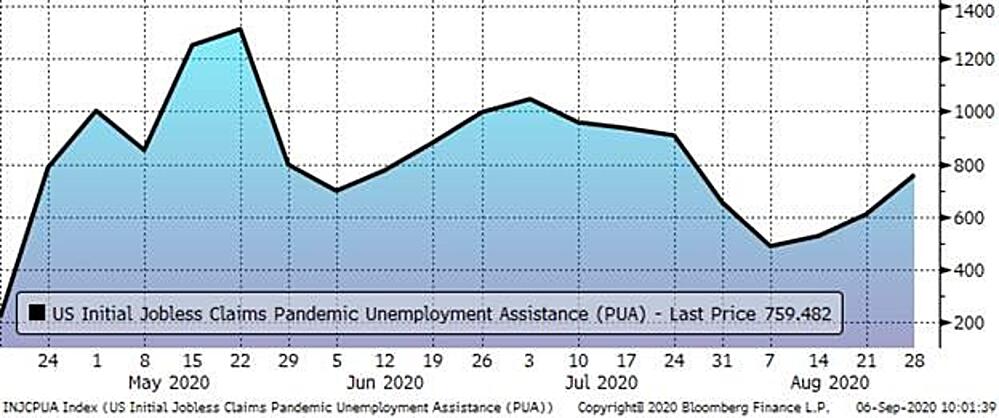

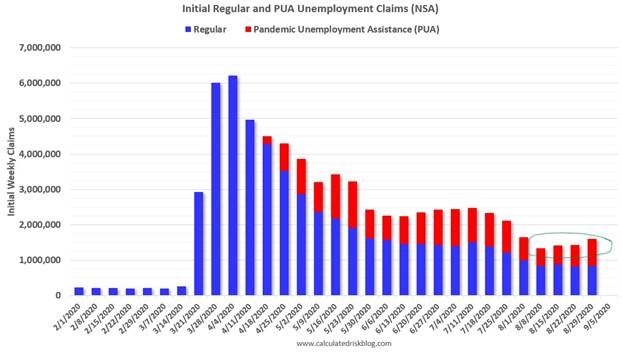

One concern – These figures do not include the data for those still receiving Pandemic Unemployment Assistance (PUA). PUA filings have been increasing weekly throughout August.

Initial Filing PUA Claims

As a result, the total employment picture has not shown much improvement over the last month.

Between February & April we lost 22 million jobs. We’ve now recovered just under half, 10.6m.

Focus of the Week – Manufacturing & Industrial

We had strong manufacturing and industrial reports for the month of August, showing that sector is on the mend. As mentioned before Rail Car Traffic and Steel are increasing.

With these surveys, a reading above 50 is a sign of expansion, below 50 is contraction.

ISM surveys were better than expected

- ISM Manufacturing Survey – 56.0 better than expected 54.8 and July’s 54.2

- ISM New Orders (a leading indicator) – very strong at 67.6 vs. expected 58.8 and July’s 61.5

- ISM Employment – 46.4 vs. July’s 44.3

- This is a sign that manufacturing jobs are still being shed, however at a slower pace and the trends are moving toward 50.

Durable Goods – 11.4%, above expectations of 11.2% and July’s 11.2%

Construction Spending – 0.1% below expected 1.0%, but better than July’s decline of -0.7%. U.S. Manufacturing PMI – 53.1, slightly below expectations of 53.6 and July’s 53.6.

Auto Sales – 15.2m cars sold, better than expectations of 14.9m and July’s 14.5m.

A Few Stories that Caught My Eye

Recent Articles

About the Author

Simeon Wallis

Simeon is the Chief Investment Officer of Aprio Wealth Management and the Director of Aprio Family Office. He brings to his role two decades of professional investing experience in publicly traded and privately held companies as well as senior-level operating and strategy consulting experience.

(470) 236-0403

Stay informed with Aprio.

Get industry news and leading insights delivered straight to your inbox.